A crypto billionaire accusing a sitting US president’s family of extortion, frozen tokens, and threats to burn $320 million in digital assets — this is either the lawsuit of the decade or the most expensive falling-out since FTX imploded.

Justin Sun, the flamboyant founder of TRON and one of crypto’s most polarising figures, has filed a federal lawsuit against World Liberty Financial (WLF), the DeFi project co-founded by Donald Trump and his son Eric. The allegations are staggering: an “illegal scheme” to seize property, blacklisted wallets, stripped voting rights, and what Sun calls a brazen extortion attempt. Welcome to the messiest divorce in decentralised finance.

The $45 Million Bet That Went Wrong

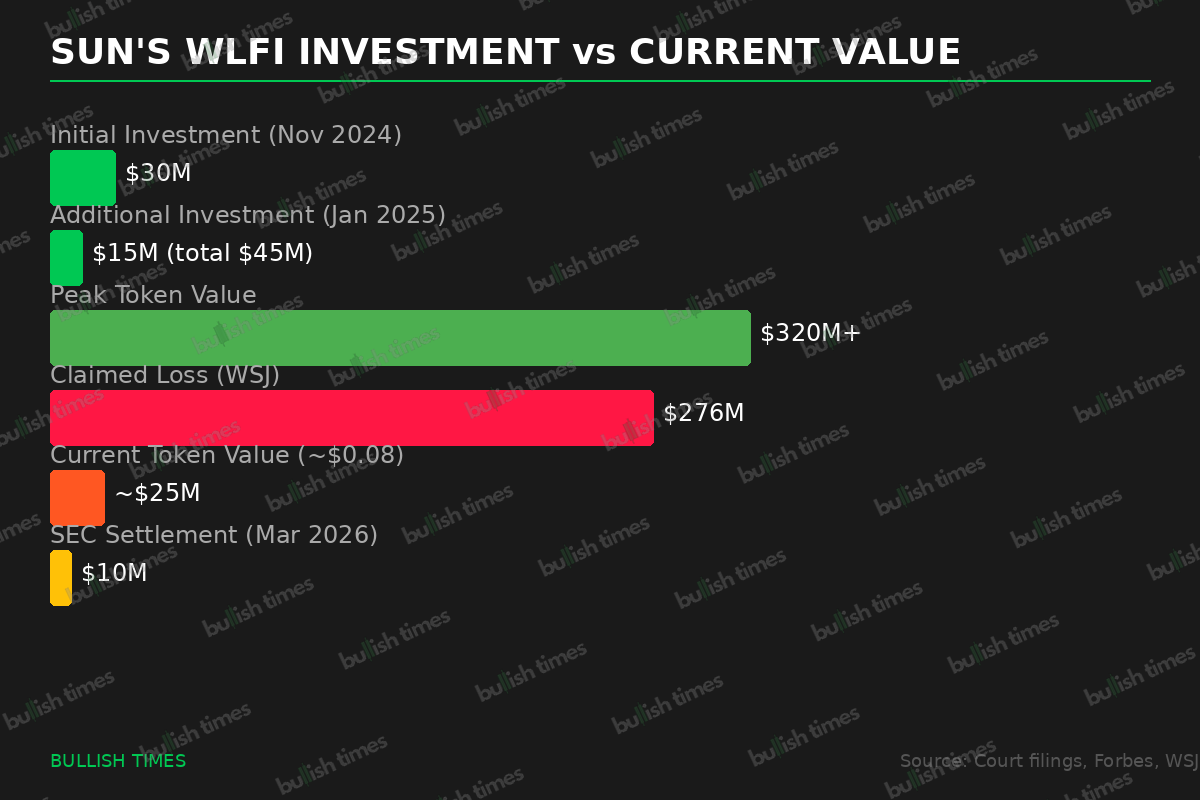

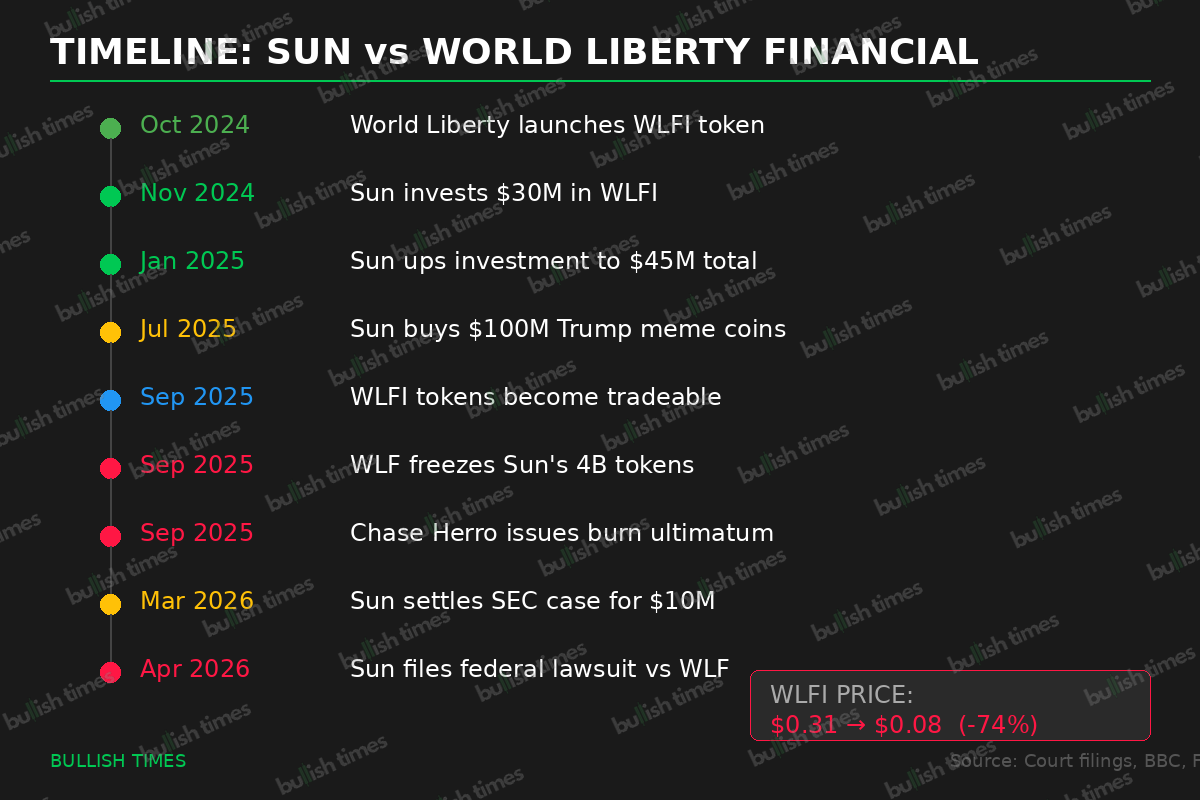

Sun’s relationship with World Liberty Financial began with optimism and enormous cheques. In November 2024, when WLFI token sales were struggling to gain traction, Sun swooped in with a $30 million investment — single-handedly rescuing the token sale from embarrassment. By January 2025, he had increased his total stake to $45 million, becoming the single largest outside investor in the Trump-backed venture.

The rationale, according to court filings, was partly ideological — Sun is an outspoken supporter of Trump’s pro-crypto stance — and partly commercial. At their peak, Sun’s 4 billion WLFI tokens were valued at over $1 billion. But the honeymoon didn’t last.

In September 2025, when WLFI tokens finally became tradeable, Sun alleges that World Liberty secretly installed smart contract mechanisms to blacklist his wallets, freeze all 4 billion of his tokens, and strip him of governance voting rights — all without notice or justification.

The Ultimatum: Surrender or We Burn Everything

The most explosive allegation centres on what Sun describes as a direct extortion attempt by Chase Herro, one of World Liberty’s co-founders. According to the complaint filed in the Northern District of California, Herro presented Sun with an ultimatum: voluntarily remove your tokens from circulation, or World Liberty will hold a governance vote to “burn” them permanently.

The threat carried weight. Sun’s filing alleges that a handful of insiders control the overwhelming majority of WLF’s voting power, making the outcome of any such vote a foregone conclusion. In essence, Sun claims he was told: comply or lose everything.

The filing further alleges that the freeze was retaliation for Sun’s refusal to mint and promote World Liberty’s USD1 stablecoin — suggesting the project’s leadership wanted to leverage Sun’s brand and capital for their own products.

Some portions of the court filing remain redacted, hinting at allegations potentially too sensitive — or too damaging — for public consumption just yet.

Both Sides Have Baggage

Let’s be clear: neither party arrives at this courtroom with clean hands.

Justin Sun settled fraud and market manipulation charges with the SEC just last month, paying a $10 million fine over allegations of wash trading the TRX token. He also bought $100 million worth of Trump’s meme coins in July 2025 — a move many interpreted as an attempt to curry favour with the administration. The SEC’s decision to drop its investigation into Sun drew sharp criticism from Senator Elizabeth Warren, who openly questioned whether the dismissal was connected to Sun’s investments in Trump-linked ventures.

On the other side, World Liberty Financial has never publicly disclosed why Sun’s tokens were frozen. CEO Zach Witkoff — whose father, Steve Witkoff, serves as Trump’s Middle East envoy — dismissed the lawsuit as a “desperate attempt to deflect attention from Sun’s own misconduct.” Eric Trump took a different approach entirely, mocking the lawsuit on X: “The only thing more ridiculous than this lawsuit is spending $6 million on a banana duct-taped to a wall.”

Neither response actually addresses the core allegation: that a project promising decentralisation secretly gave itself the power to freeze and destroy a major investor’s holdings.

The Bigger Picture: DeFi’s Decentralisation Illusion

Beyond the personalities and the drama, this case strikes at something far more fundamental. World Liberty Financial marketed itself as a decentralised governance platform where token holders had meaningful power. Sun’s lawsuit alleges the exact opposite — that insiders retained unilateral control to blacklist wallets, freeze assets, and override governance at will.

If those allegations hold up, it raises uncomfortable questions for the entire DeFi sector. How many supposedly decentralised protocols have similar kill switches lurking in their smart contracts? How many governance tokens are truly governance tokens when a handful of wallets control the outcome of every vote?

The WLFI token itself tells a grim story. From a September 2025 high of $0.31, it has cratered 74% to roughly $0.08 — wiping out billions in combined investor value. Sun’s filing goes so far as to suggest World Liberty may be on the “brink of collapse and potential insolvency.”

What Happens Next

The lawsuit was filed on Tuesday in the Northern District of California. World Liberty has signalled it intends to seek dismissal, but given the involvement of a sitting president’s family, the political dimensions alone could keep this in the headlines for months.

Sun has been careful to frame the lawsuit as targeting “certain individuals” rather than Trump himself — a strategic manoeuvre that leaves the door open for a settlement while avoiding a direct confrontation with the most powerful man in America.

But make no mistake: this case has the potential to become crypto’s most politically charged legal battle since the SEC went after Ripple. A billionaire with a fraud settlement accusing a president’s son of extortion, frozen tokens worth hundreds of millions, and a DeFi project that may have never been decentralised at all.

You couldn’t write this script. But then again, crypto never needed scriptwriters.

This is a developing story. Bullish Times will continue to track the Sun v. World Liberty Financial case as further filings become public.