The most powerful banker in America has drawn a line in the sand. Jamie Dimon wants crypto’s biggest legislative victory killed — and he’s willing to burn Washington’s fragile bipartisan consensus to do it.

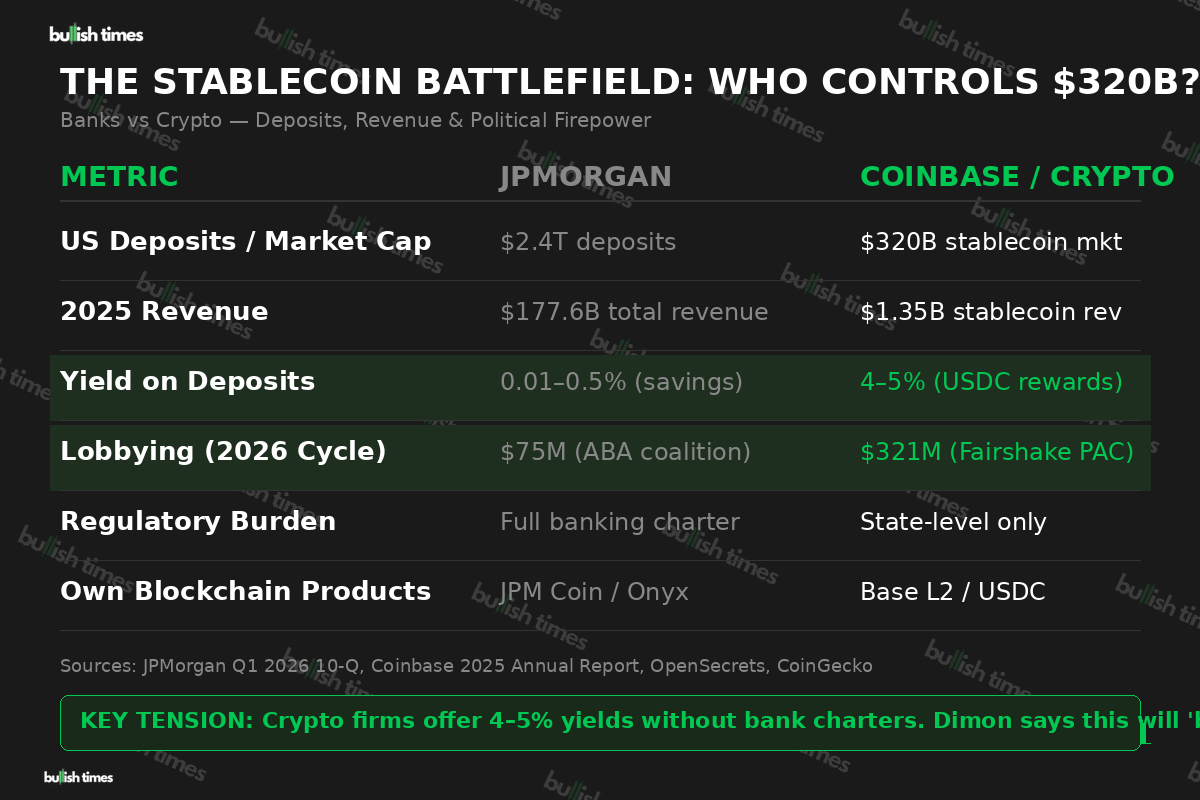

The JPMorgan Chase chief executive went on Fox Business last week and did something extraordinary: he publicly threatened to mobilise the entire US banking sector against the Digital Asset Market Clarity Act, the most ambitious crypto regulation bill in American history. His target? Coinbase CEO Brian Armstrong. His weapon? The combined lobbying firepower of JPMorgan, the American Bankers Association, community banks, and credit unions. The stakes? A $320 billion stablecoin market that Wall Street increasingly views as an existential threat to its deposit monopoly.

Dimon’s Declaration: ‘It Will Blow Up’

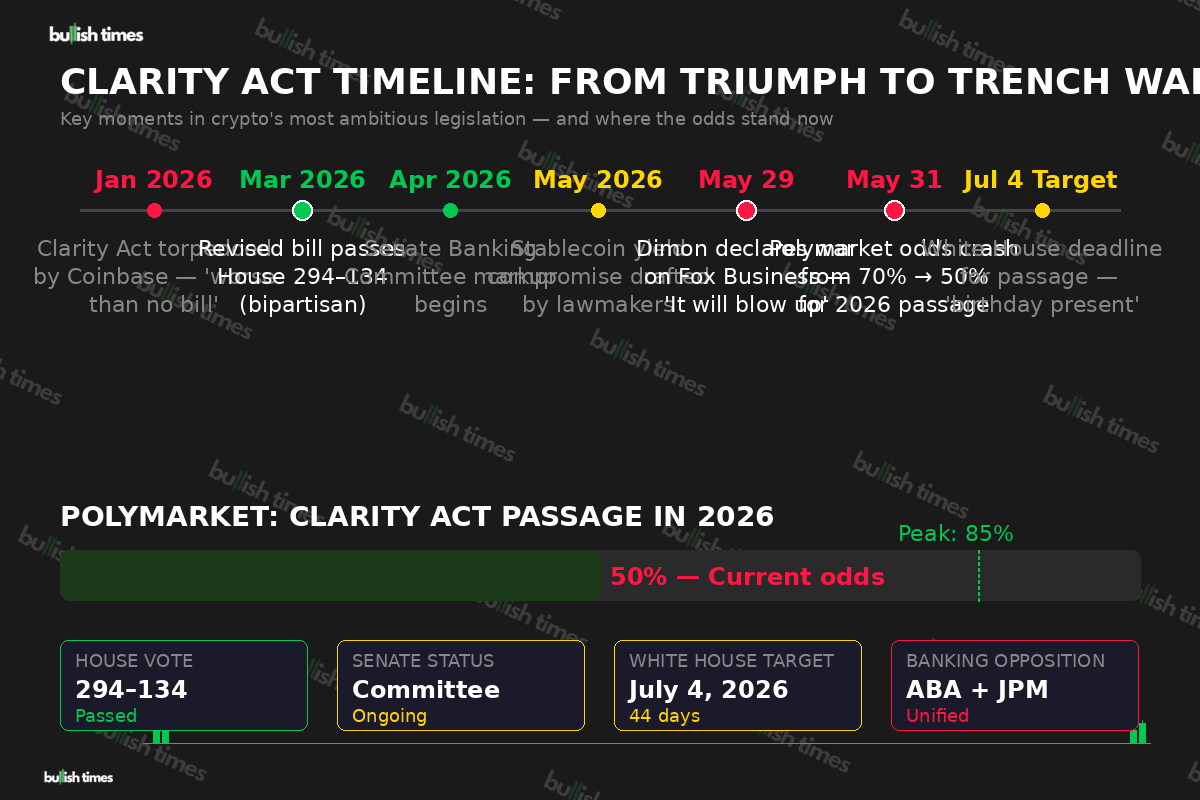

The CLARITY Act sailed through the House of Representatives with a commanding 294–134 bipartisan majority. The White House set a July 4 deadline — Patrick Witt, executive director of the president’s council of advisors for digital assets, called it “a tremendous birthday present for America” at the Consensus conference in Miami.

Then Dimon detonated a grenade into the Senate negotiations.

“The banks will not accept it that way,” he told Fox Business. “I’m not worried about stablecoins but if it happened I’m telling you I will have nothing to do with it and it will eventually blow up.”

His fury centres on stablecoin yield. The current draft permits crypto firms to offer interest-like rewards on stablecoin balances — effectively replicating bank savings accounts without the regulatory overhead of a federal banking charter. No capital adequacy requirements. No mandatory liquidity coverage ratios. No fractional reserve mandates.

For banks paying depositors 0.01% to 0.5% whilst crypto platforms offer 4–5% on USDC, this is not a policy disagreement. It is economic war.

The Hypocrisy at the Heart of Wall Street’s Rage

Here is the delicious irony Dimon would rather you ignored: JPMorgan is aggressively building its own blockchain infrastructure. The bank’s Onyx division runs JPM Coin for institutional settlements. Its tokenised money market funds stream yields directly to enterprise clients. JPMorgan wants blockchain-powered products for the wealthy whilst ensuring retail investors cannot access the same technology through crypto-native platforms.

Dimon went directly after Armstrong personally. “No one’s gonna bow down to him, or Coinbase,” he told Politico. “He’s the only one and he’s spending hundreds of millions of dollars in Washington on this thing.”

He’s not entirely wrong on the numbers. Crypto super PACs, led by Fairshake, have amassed over $321 million in the 2026 cycle — outspending pharmaceutical and defence lobbying groups. But the banking industry’s own ABA coalition has deployed approximately $75 million fighting the bill.

Coinbase fired back through chief policy officer Faryar Shirzad, arguing consumers actively support rewards programmes and clear regulatory rules. The subtext: banks are not fighting to protect consumers. They are fighting to protect a deposit moat eroding since stablecoins proved you can move dollars globally, instantly, for fractions of a penny.

A Bill on Life Support?

The political fallout has been swift. On Polymarket, the odds of the CLARITY Act becoming law in 2026 have cratered from approximately 85% to just 50% — a coin flip for what was once near-certain legislation.

In January, Coinbase itself torpedoed an earlier version, with Armstrong declaring it “worse than no bill.” A revised version powered through the House in March. The Senate Banking Committee began markup in April. Lawmakers hammered out a stablecoin compromise in May banning rewards “economically or functionally equivalent” to deposit interest.

Then Dimon’s intervention changed the calculus entirely.

The Real Question Dimon Won’t Answer

Strip away the lobbying and the theatrical warnings, and you arrive at a simple question: why should banks be the only institutions allowed to custody and lend dollars?

The stablecoin market has reached $320 billion. Transaction volumes hit $46 trillion in 2025 — more than 20 times PayPal’s annual volume. USDT alone commands $189 billion in market capitalisation. These are not toys. They are monetary infrastructure operating 24/7 without bank holidays, wire delays, or $35 overdraft fees.

Dimon’s “it will blow up” prediction carries an uncomfortable echo. Wall Street’s resistance to every significant financial innovation — from fintech lending to payment apps to open banking — has followed an identical playbook: warn of systemic risk, mobilise regulators, buy time to build a proprietary alternative.

The difference this time: crypto has $321 million in political ammunition and a White House that has staked its credibility on delivering legislation before Independence Day. The banking lobby has institutional weight. Crypto has momentum.

With 44 days until the deadline and Polymarket giving even odds, the CLARITY Act has become the most important piece of financial legislation in a generation — and its fate rests on whether Congress bows to the man who runs America’s largest bank or the industry that wants to replace him.

This story is developing. The Senate Banking Committee is expected to resume negotiations this week.