Six weeks into Britain’s most significant overhaul of retail investment disclosure in a decade, the new Consumer Composite Investments regime is quietly reshaping how products reach UK consumers — and overseas firms ignore it at their peril.

The CCI framework, which came into force on 6 April 2026, replaces the long-criticised PRIIPs KID and UCITS KIID requirements with a single, UK-specific disclosure regime. It is not merely a rebrand. For any firm — domestic or foreign — that manufactures or distributes investment products to British retail investors, the rules of engagement have fundamentally changed.

Out With the Templates, In With the Consumer Duty

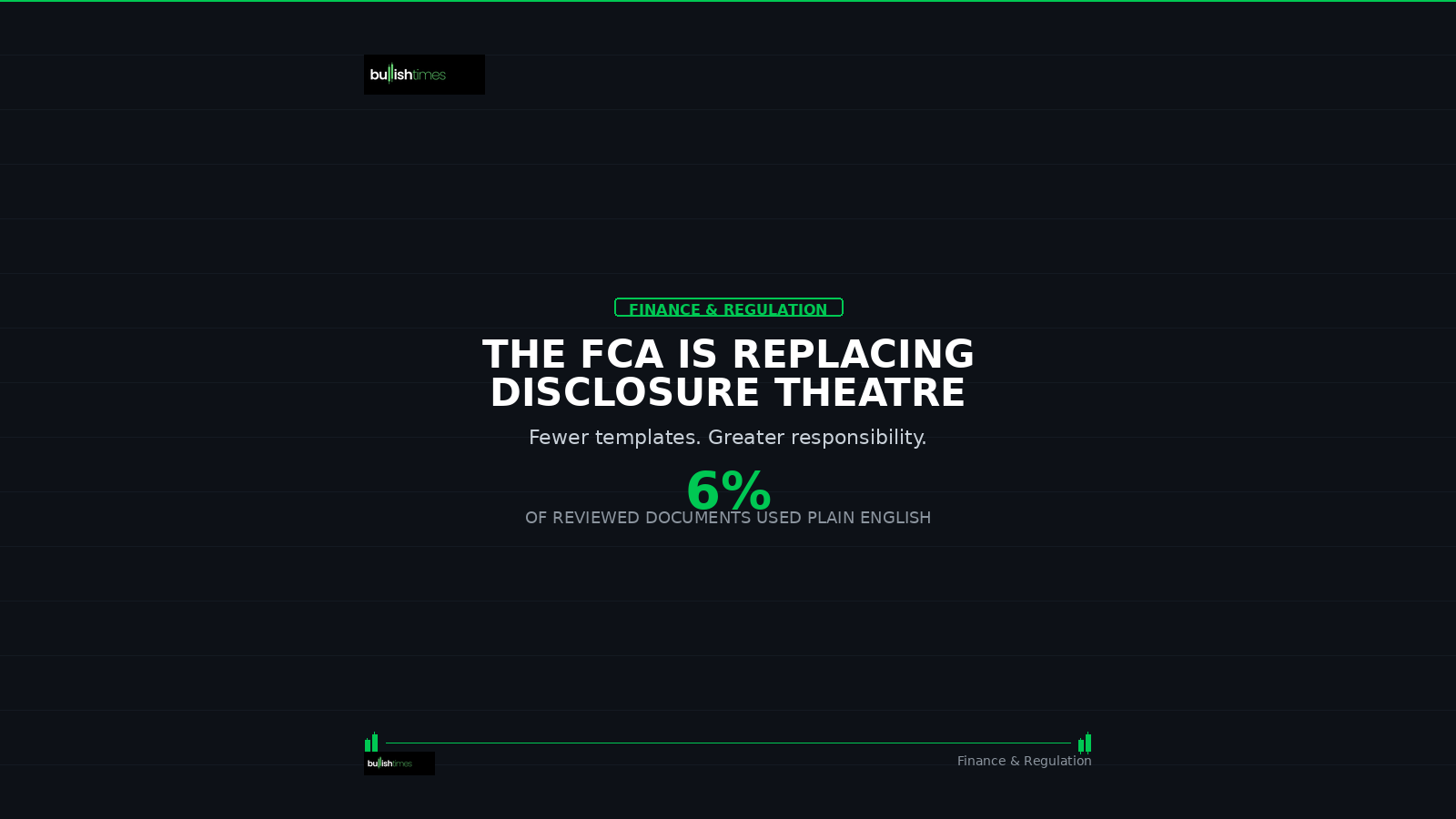

The old PRIIPs regime was nobody’s favourite piece of regulation. Inherited from EU legislation and onshored after Brexit, it mandated rigid Key Information Documents that prioritised box-ticking over genuine consumer understanding. The FCA’s own consultations found that retail investors frequently struggled to extract meaningful information from the prescribed format.

The CCI regime takes a markedly different approach. Rather than imposing a fixed template, it requires manufacturers to produce a consumer-friendly product summary covering costs, risks, returns, and past performance — but grants considerable flexibility in how that information is presented. The catch, and it is a significant one, is that everything must demonstrably satisfy the Consumer Duty. Firms cannot simply redesign their old KIDs and call the job done. The FCA has been explicit: the key risk is producing disclosures that technically comply but fail Consumer Duty.

The product scope is broadly familiar — open-ended and closed-ended funds, structured products and deposits, contracts for difference, insurance-based investment products — but the regime consolidates everything under a single framework. A standardised 1–10 risk score replaces the previous summary risk indicator, and past performance must be shown on a line graph based on an initial £10,000 investment over up to ten years.

The Overseas Firm Question

Here is where it gets genuinely interesting for the cross-border market. The FCA has explicitly confirmed that the CCI regime applies to overseas firms that wish to promote products to UK consumers. This is not a suggestion — it is a regulatory statement.

For Swiss, European, or other non-UK manufacturers of structured products, actively managed certificates, or fund interests aimed at UK retail investors, this creates a clear obligation. If the product meets the CCI definition — broadly, any investment where the return depends on the performance of underlying or reference assets not directly purchased by the investor — and it is directed at UK retail clients, the disclosure rules apply regardless of where the manufacturer sits.

The transition period offers some breathing room. Until 8 June 2027, manufacturers can choose between the new CCI product summary and their existing disclosure documents. Operators of Overseas Funds Regime recognised schemes benefit from the same flexibility. But the direction of travel is unambiguous: by next summer, the old documents will no longer suffice.

Firms that distribute exclusively to wholesale or institutional investors, or that clearly mark their communications as not for retail, remain outside scope. The regime explicitly carves out products distributed to non-retail investors or to investors outside the United Kingdom. For firms operating under the Berne Financial Services Agreement — which permits FINIG-licensed Swiss firms to serve UK wholesale clients with net assets above £2 million — the CCI regime may not bite directly. But any ambition to reach UK retail investors, whether now or in the future, requires CCI readiness.

The Broader Regulatory Picture

The CCI regime does not exist in isolation. It arrives alongside the FCA’s 2026 Regulatory Priorities, published in March, which replaced the previous Dear CEO letters with nine sector-specific reports. The wholesale buy side report is particularly instructive: the FCA expects firms to establish clear accountability and governance for emerging technologies, embed the Consumer Duty across distribution chains, and maintain robust oversight of appointed representatives.

The emphasis on Consumer Duty is relentless. The FCA will continue using data to identify outlier firms, and has signalled focused work on private markets, model portfolio services, and retirement income products. For overseas firms, the message is consistent: if you touch UK retail, you play by UK rules.

The FCA is also consulting on cryptoasset perimeter guidance (consultation closes 3 June 2026) and implementing a new short selling regime from 13 July 2026. The regulatory tempo is, by any measure, brisk.

For firms with cross-border ambitions, the practical questions are straightforward but require prompt attention. Confirm whether your products fall within the CCI definition. Establish whether you are a manufacturer, distributor, or both. Begin designing product summaries that genuinely serve consumer understanding — not just regulatory compliance. And test them: the FCA has specifically mentioned focus groups, comprehension surveys, and readability assessments as evidence that firms take the Duty seriously.

The eighteen-month transition window may feel generous today. By the time systems, governance, and documentation are aligned, it will feel rather less so.