A three-employee company just became the largest Ethereum holder on Earth — and it’s haemorrhaging ten billion dollars while doing it.

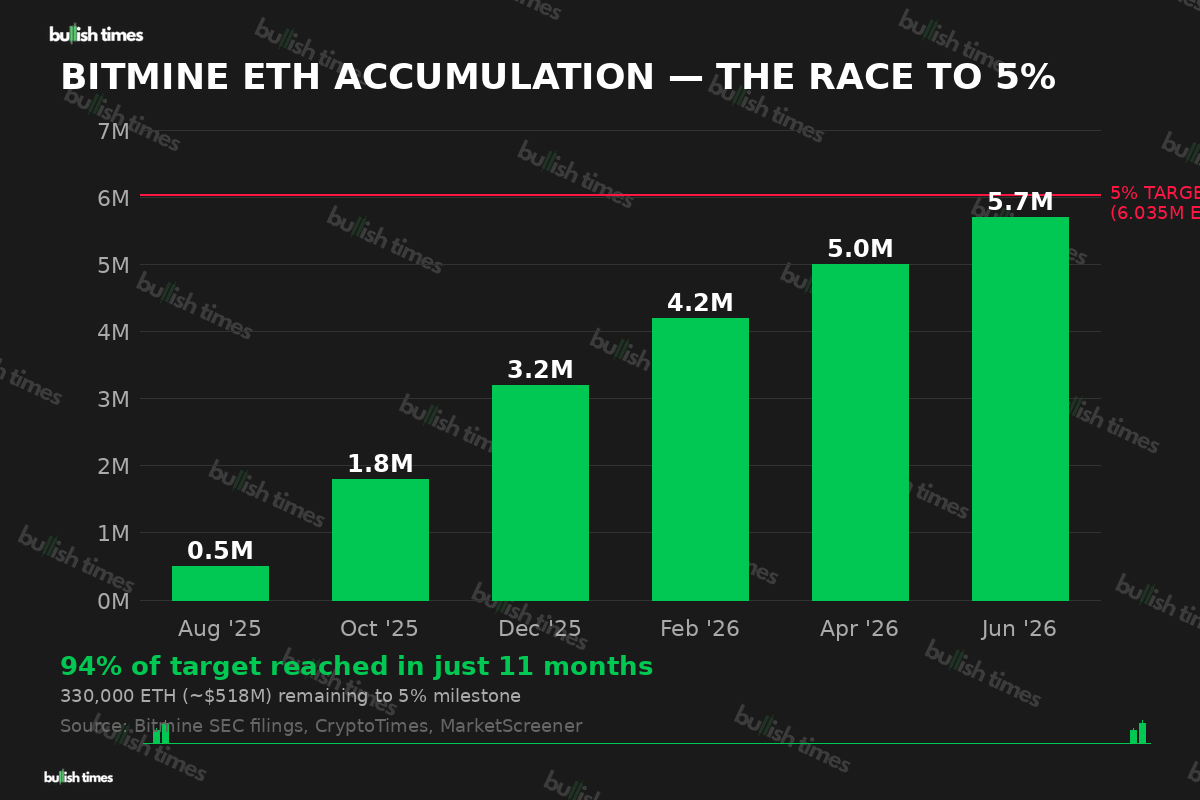

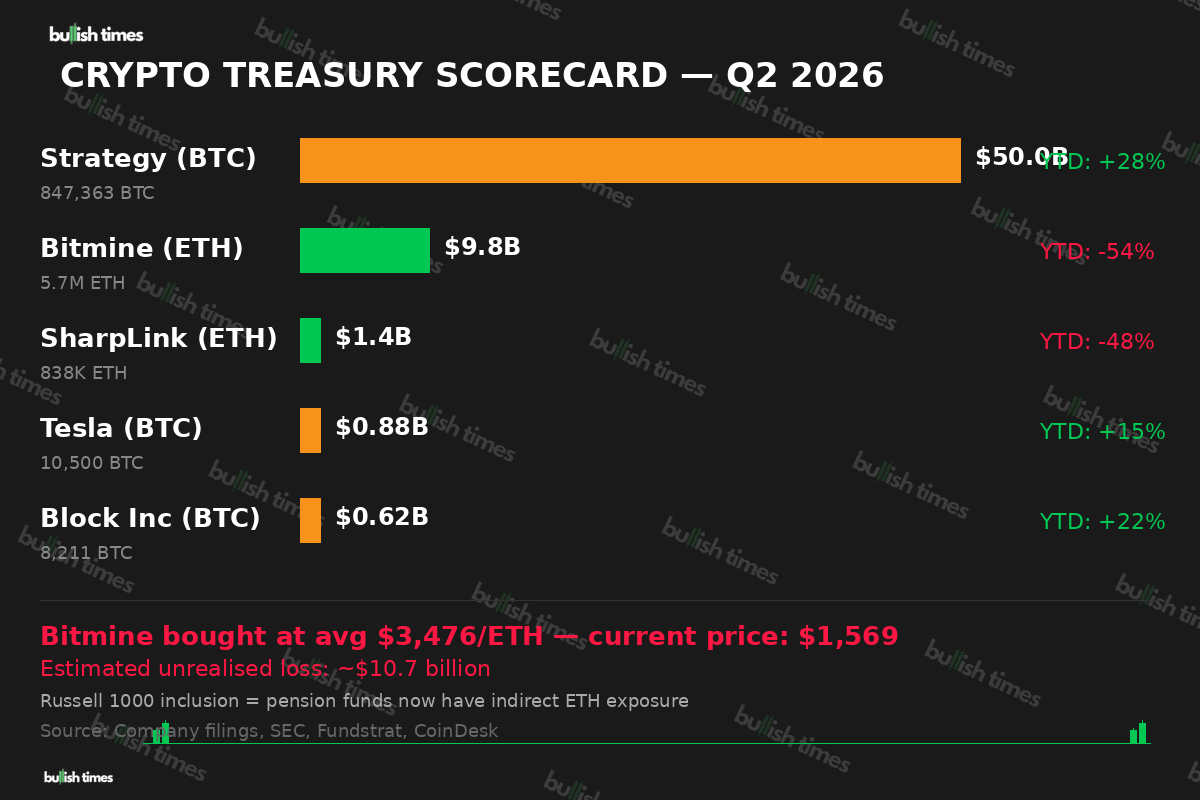

Bitmine Immersion Technologies, chaired by Fundstrat’s Tom Lee, disclosed on 29 June that its crypto treasury has swollen to $9.8 billion. The centrepiece: 5.7 million ETH, representing 4.7% of Ethereum’s entire circulating supply. The firm is 94% of the way to its stated goal of owning 5% of all Ethereum — a target Lee has branded the “Alchemy of 5%.” The catch? It bought most of that stack at an average price of $3,476 per token, and ETH currently trades at roughly $1,569.

The Alchemy of 5% — by the Numbers

Bitmine pivoted from Bitcoin mining to an Ethereum-focused treasury model in mid-2025, and the pace of accumulation has been staggering. The company added another 27,084 ETH last week alone — roughly $43 million in fresh purchases — even as Ethereum tumbled 10% over the same period. In 11 months, Bitmine has gone from negligible ETH holdings to a position that dwarfs every other corporate Ethereum treasury in existence.

Of those 5.7 million tokens, 4.88 million are staked through MAVAN (Made in America VAlidator Network), Bitmine’s proprietary staking platform. Annualised staking revenue currently projects at $211 million, rising to $246 million once the full treasury is deployed. Bitmine claims it has staked more ETH than any other single entity on the planet.

The unrealised loss is eye-watering. At a reported average acquisition cost near $3,476 per ETH, and current prices around $1,569, Bitmine is carrying an estimated $10.7 billion paper loss — one of the largest in corporate crypto history. Under FASB fair-value accounting rules, those swings flow directly through GAAP earnings, producing multi-billion-dollar quarterly losses that would send most boards into cardiac arrest.

Russell 1000 — Your Pension Now Holds Ethereum

On 26 June, Bitmine was added to the Russell 1000 Large-Cap Index, a benchmark tracked by passive funds managing trillions of dollars. The Investment Company Institute estimates that passive investment vehicles typically represent 18–20% of a company’s shares. This means pension funds, 401(k) plans, and retirement accounts benchmarked to the Russell 1000 will now carry indirect exposure to Ethereum through their BMNR allocation — whether or not their managers intended to hold crypto-linked equities.

Tom Lee framed the inclusion as a watershed. “Being added to the Russell 1000 is expected to add hundreds, and possibly thousands, of additional institutional investors as equity owners of Bitmine,” he stated. Critics see it differently: the world’s largest accumulator of a volatile asset, staffed by three people, is about to funnel Ethereum exposure into grandma’s retirement fund.

Bitmine also raised $273.8 million through a preferred stock offering in June, with weekly dividend payments tied directly to staking revenue. The Series A Perpetual Preferred Stock trades on the NYSE under BMNP at a 9.5% yield — a structure that weds shareholder income to the health of Ethereum’s proof-of-stake system. If staking yields contract or ETH continues to slide, the maths get uncomfortable quickly.

Strategy’s ETH Twin — or Something Riskier?

Comparisons with Michael Saylor’s Strategy (formerly MicroStrategy) are inevitable, but the differences matter. Strategy’s Bitcoin treasury sits at roughly $50 billion across 847,363 BTC — a position that is currently in profit. Bitmine’s ETH treasury is worth approximately $8.9 billion and deep underwater.

ETH itself is down roughly 50% since January and nearly 60% from its all-time high, making the Strategy comparison less flattering by the month. SharpLink Gaming, another corporate Ethereum buyer, added 39,196 ETH ($62.4 million) over just three days last week, whilst spot ETH ETFs recorded a seventh consecutive week of net outflows. The divergence is stark: corporate treasuries are buying hand over fist whilst institutional fund flows point the other direction.

Tom Lee has called drawdowns “a feature, not a bug” of the long-term treasury approach. He attributed recent selling to quarter-end window-dressing rather than structural weakness, pointing to positive developments including the launch of Ethlabs — an independent R&D organisation co-funded by Bitmine and staffed by five former Ethereum Foundation researchers — and the Bank of England’s revised stablecoin framework.

The Concentration Question

Bitmine’s accumulation raises a question that sits at the intersection of DeFi philosophy and traditional finance risk management: what happens when a single corporate entity controls nearly 5% of a supposedly decentralised network’s supply?

With 4.88 million ETH staked, Bitmine commands an outsized share of Ethereum’s validator set. If the company ever needed to raise cash — through debt, equity dilution, or outright ETH sales — the selling pressure could be catastrophic for a market already struggling with thin liquidity. Concentrated ownership supports prices whilst the buying continues, but it also builds a single point of failure into an ecosystem that was designed to have none.

BMNR stock has gained over 260% in the past year but is down 49% year-to-date, currently trading at $13.80 — miles from its 52-week high near $161. The stock often trades at or below net asset value, offering leveraged ETH exposure for the adventurous but amplifying downside risk for everyone else.

Bitmine needs roughly 330,000 more ETH — about $518 million at current prices — to hit its 5% target. At its current accumulation pace, the “Alchemy of 5%” milestone could arrive within weeks. Whether that proves to be the greatest corporate treasury play in crypto history or the most expensive depends entirely on a question nobody can answer: where Ethereum trades six months from now.

Bitmine’s weekly treasury updates are filed with the SEC. This story will be updated as new data emerges.