Nearly 1,700 British retail investors have launched a landmark class-action lawsuit against the world’s largest crypto exchange, claiming Binance sold them high-risk derivative products it had no legal right to offer. The price tag: at least £150 million.

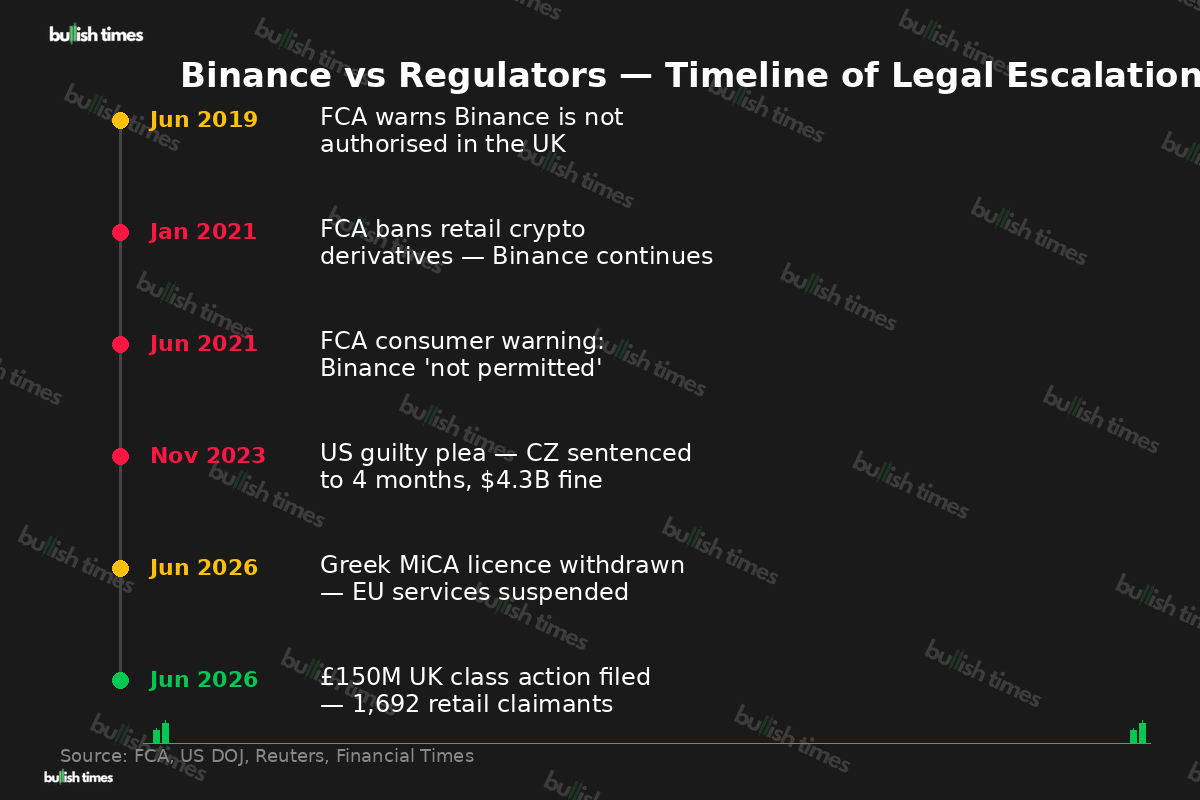

The group claim, filed in London’s High Court on 29 June 2026, names Binance Holdings, founder Changpeng “CZ” Zhao, Abu Dhabi-registered Nest Exchange, and unnamed “Persons Unknown” who operated the Binance trading platform. It is the first case of its kind in the United Kingdom involving the unauthorised sale of crypto derivatives to retail users — and the legal implications stretch far beyond these 1,692 claimants.

What the Claimants Allege

The lawsuit, brought by law firm KP Law on behalf of lead plaintiff Tomas Sutas, centres on a straightforward but legally devastating allegation: Binance offered leveraged tokens, cryptocurrency futures, options, and margin trading products to UK retail customers from around September 2019 — without ever holding authorisation from the Financial Conduct Authority.

Under the Financial Services and Markets Act 2000 (FSMA), selling regulated financial products without proper authorisation can render contracts unenforceable. That legal mechanism is precisely what the claimants are leveraging, arguing they are entitled to recover money paid and compensation for losses suffered.

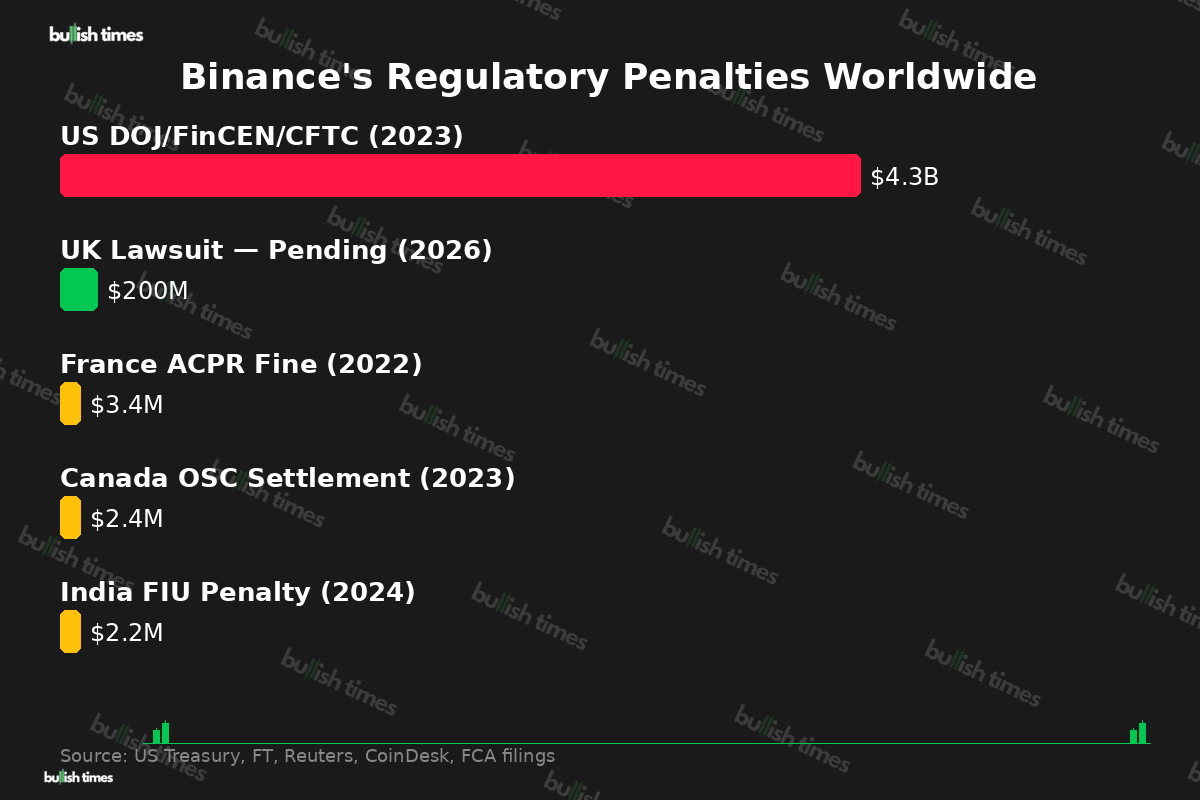

KP Law partner Hannah Sharp told the Financial Times the firm’s clients had suffered devastating financial losses. One claimant, financial controller Tomas Sutas, invested more than $132,000 in Binance derivatives and lost everything. Others reportedly lost tens of thousands of pounds. The total damages sought exceed £150 million — roughly $200 million at current exchange rates.

The FCA Ban Binance Allegedly Ignored

The timeline makes uncomfortable reading for Binance. The FCA banned the sale, marketing, and distribution of crypto derivatives to retail consumers in January 2021, estimating the ban would save retail investors approximately £53 million per year. The regulator cited extreme volatility and the high probability of sudden, catastrophic losses.

The claimants allege Binance continued promoting and selling these products to UK users even after the ban took effect. According to KP Law, “there was no effective barrier preventing UK clients from accessing these products.” Binance took some steps to restrict UK access — requiring users to complete additional verification — but the plaintiffs argue these measures were cosmetically inadequate.

The Binance UK lawsuit raises a fundamental question about crypto exchange responsibility: when an unlicensed platform sells high-risk products to retail investors, who bears the cost of their losses — the platform or the trader?

CZ’s Legal Shadow Grows Longer

This is not CZ’s first courtroom appearance in a regulatory context. In November 2023, Binance pleaded guilty to US money laundering and sanctions violations, resulting in a record $4.3 billion settlement with the Department of Justice, FinCEN, OFAC, and the CFTC. CZ personally served a four-month prison sentence before receiving a presidential pardon from Donald Trump.

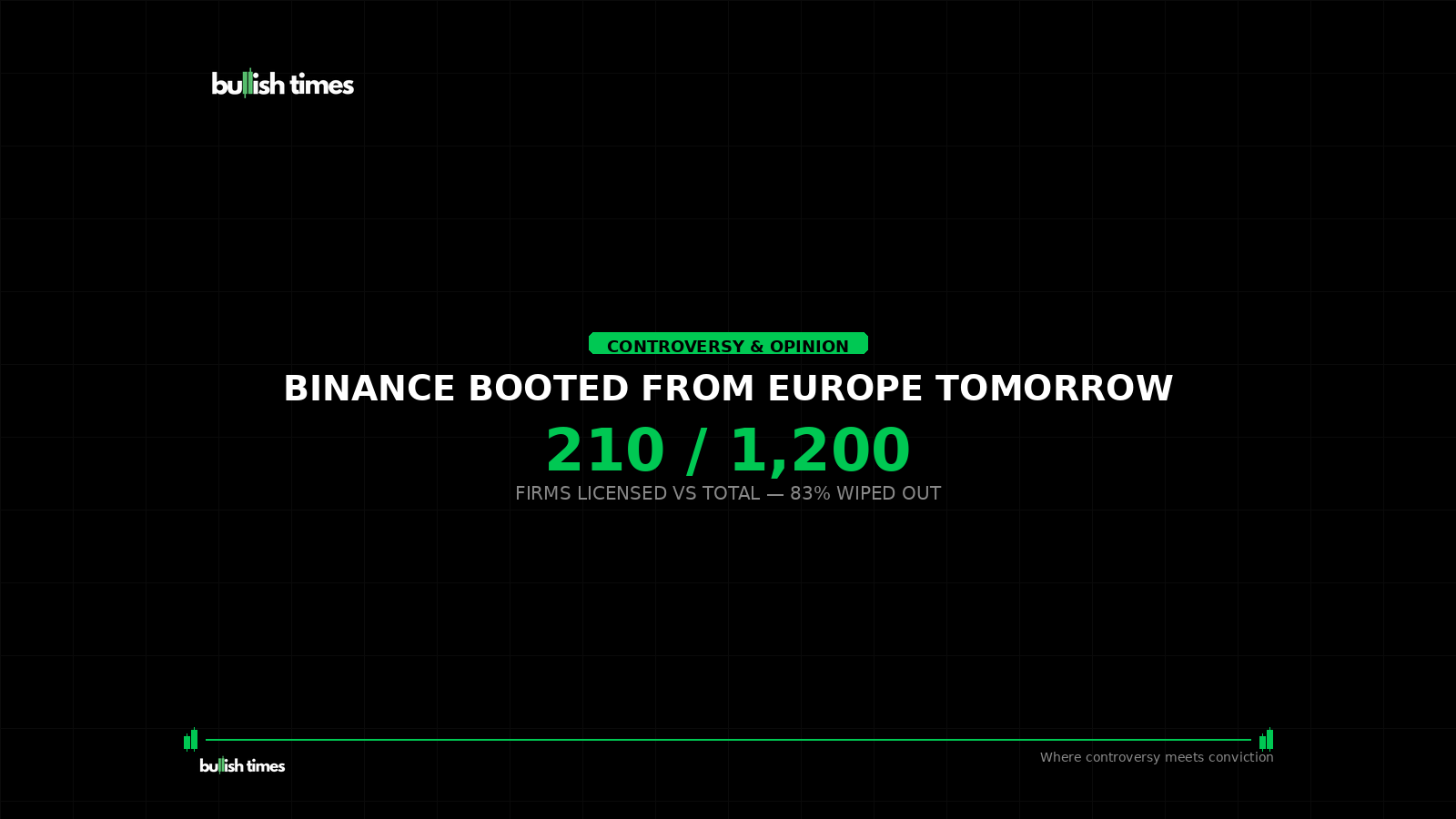

The timing of the UK lawsuit is particularly sharp. It landed just days after Binance withdrew its application for a Greek MiCA licence, effectively losing access to European Union customers from 1 July 2026. CZ insisted the application had been “fully compliant” before unnamed political forces intervened, but the result is the same: Binance is now locked out of the EU, facing a £150 million lawsuit in London, and still operating under a five-year US monitorship.

The pattern is unmistakable. Jurisdiction after jurisdiction — the United States, the European Union, and now the United Kingdom — is tightening the vice on an exchange that grew to dominance by moving faster than regulators could follow.

The Precedent That Could Reshape Crypto in the UK

If the London High Court finds that Binance’s crypto derivatives qualified as regulated financial instruments under FSMA — and that selling them without authorisation renders the transactions voidable — the implications extend well beyond this case.

The FCA recently unveiled its long-awaited comprehensive regulatory framework for crypto, requiring firms to meet financial safety standards, comply with anti-money laundering laws, and satisfy consumer protection requirements. A successful outcome for the claimants would effectively confirm that the old rules already applied — that crypto exchanges could not operate outside the perimeter simply by claiming their products were not traditional securities.

That precedent could open the floodgates. Binance was far from the only exchange offering leveraged crypto products to UK retail customers during the period in question. If the legal template established here holds, similar actions against other platforms become not just possible but probable.

Binance’s response has been measured. “Strict compliance with UK regulations is a top priority for Binance,” a spokesperson stated. “We will defend against these claims through the appropriate legal process in due course.” The exchange has not addressed the specific allegations.

For the 1,692 claimants — many of whom lost their savings chasing leveraged returns on a platform they believed was operating legitimately — the legal process cannot move fast enough.

This is a developing story. Bullish Times will continue to track the London High Court proceedings as they unfold.