India’s central bank has had enough. While the rest of the world races to regulate crypto, the Reserve Bank of India is quietly building the legal case to bury it — and 39 million investors are in the crosshairs.

Reuters obtained internal government documents from May and June 2026 that reveal what India’s crypto industry has feared for years: the RBI isn’t waiting for a law. It’s pushing for a policy that “leans towards prohibition.” The documents, reviewed exclusively by the news agency, show the central bank urging that banks and financial institutions be barred from holding, trading or gaining any exposure to crypto assets and privately issued stablecoins.

This is not a new regulatory framework. It is the groundwork for a ban.

The Internal Documents That Changed Everything

India has existed in crypto’s grey zone since 2018, when the Supreme Court struck down an earlier RBI-driven banking ban that had effectively choked the industry. A 2021 bill to outlaw private cryptocurrencies was drafted, debated, and then quietly shelved. The government kept repeating its preferred line: any plan must “balance innovation with risk management.”

Those documents tell a different story. The RBI’s stance, according to sources familiar with the central bank’s thinking who spoke to Reuters, is “towards prohibition” — keeping crypto firmly outside the regulated financial system. Internal discussions between the finance ministry and the RBI, which had moved in September 2025 towards limited regulatory clarity, appear to have reversed course. The tone has hardened.

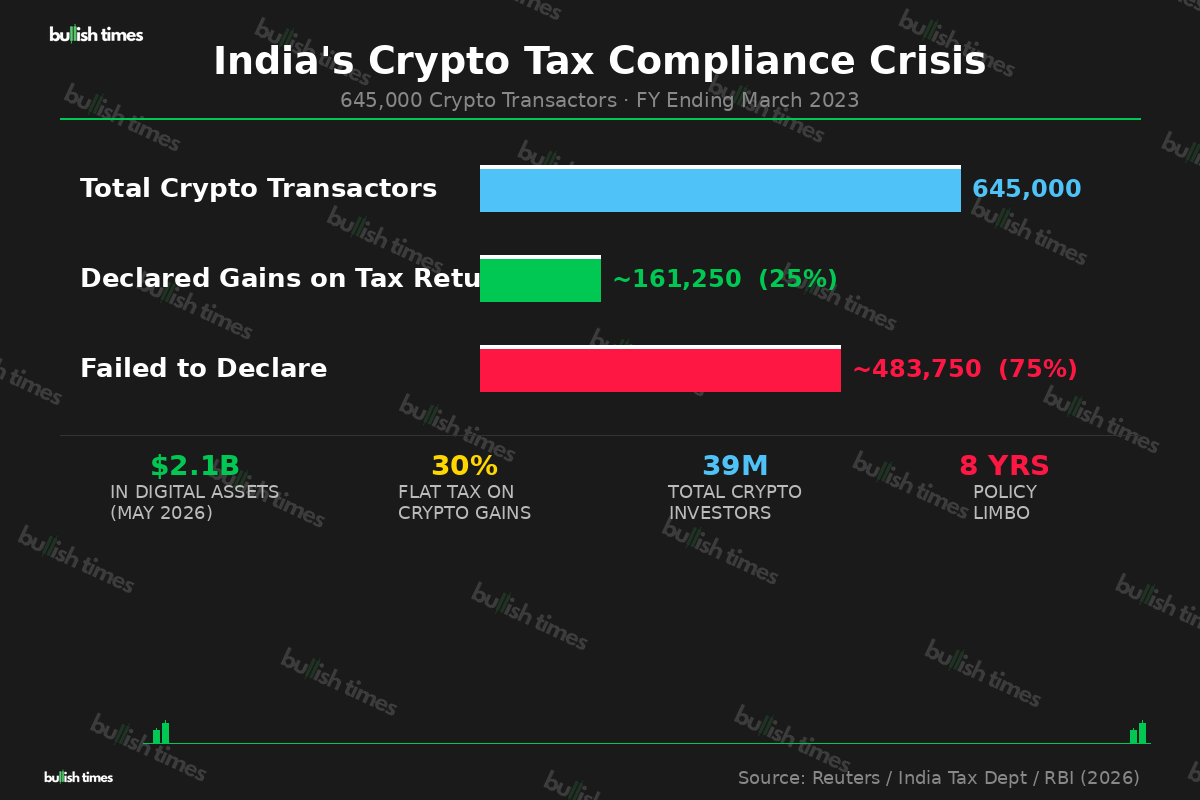

The trigger? Compliance. India’s tax department, which already taxes crypto gains at a punishing flat rate of 30%, has found something alarming: fewer than a quarter of the 645,000 individuals who made cryptocurrency transactions in the financial year ending March 2023 actually declared those gains on their tax returns. That is a compliance failure rate of roughly 75%. The department also flagged that transactions routed through offshore exchanges, private wallets, and rupee-denominated peer-to-peer trades make taxable income nearly impossible to track.

The Stablecoin Problem Nobody Saw Coming

The RBI’s hostility extends beyond volatile tokens. The central bank has now taken aim at stablecoins too — and the reasoning is striking in its bluntness.

Foreign-currency-backed stablecoins, the RBI argues, pose a direct threat to India’s monetary sovereignty. Rupee-backed tokens would erode the government’s seigniorage income — the revenue it derives from issuing its own currency — and could create dangerous instability during market stress. Most damaging of all: if holders can stay in stablecoins indefinitely without converting back to rupees, they can sidestep India’s 30% crypto gains tax entirely. The RBI doesn’t just view stablecoins as risky. It views them as a tax evasion engine.

India’s Ministry of Corporate Affairs is separately reviewing accounting standards for virtual digital assets, according to the same documents. The machinery of prohibition is being built quietly, piece by piece.

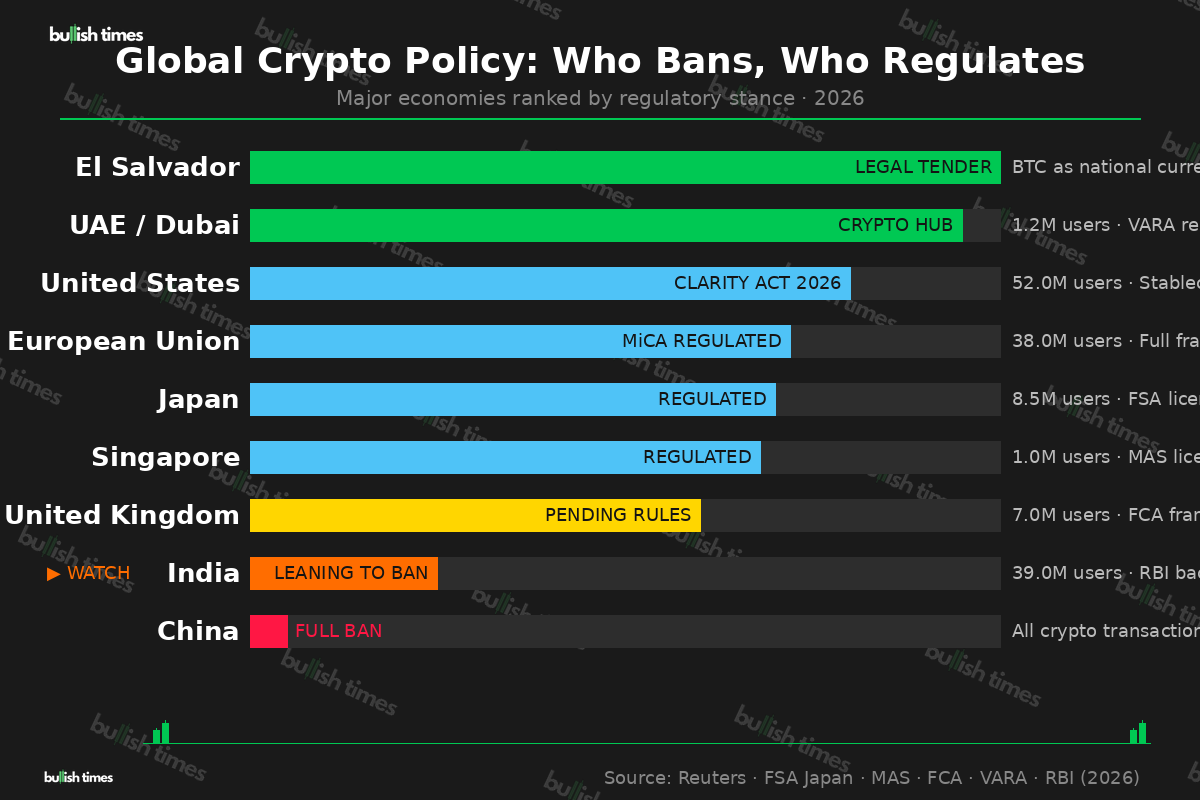

India vs the World: Swimming Against the Tide

The timing is extraordinary. The RBI is doubling down on restriction at the precise moment that crypto is winning its most significant regulatory battles globally.

The United States passed stablecoin legislation under the CLARITY Act in 2026. The European Union’s MiCA framework is now fully live. Japan and Singapore have both established comprehensive licensing regimes that allow crypto to operate legally under regulated conditions. Even the UAE has built an entire regulatory hub — the Virtual Assets Regulatory Authority — to attract the industry.

India, which has 39 million crypto traders holding approximately $2.1 billion in digital assets, sits at a crossroads. Follow China’s 2021 playbook — a total ban that pushed the industry underground and offshore — or build the framework that every other major democracy is now implementing.

The documents suggest the RBI wants the China option.

What the RBI Gets Wrong

The tax compliance argument is real. A 75% non-declaration rate is genuinely alarming for any finance ministry. But the RBI’s proposed solution — prohibition — has already been road-tested. It doesn’t work.

Academic research cited in the same documents found that India’s 2018 banking ban cut retail crypto downloads and users by roughly 60%. It did not eliminate trading. It pushed it offshore, to exchanges and wallets beyond Indian jurisdiction, where tax enforcement is even harder. The very problem the RBI claims it is trying to solve — untraceable offshore transactions — is the predictable outcome of the policy it is now pushing.

Meanwhile, the industry is watching global exchanges. Binance and Coinbase are permitted to operate in India after registering with the government’s anti-money-laundering unit. The moment a formal ban is imposed, those registrations evaporate — and India’s 39 million traders lose access to legitimate, trackable platforms and migrate to exactly the offshore, unregulated environment the RBI fears most.

The Verdict: History Repeating

India has been here before. In 2018, the RBI tried to kill crypto through the banks. The Supreme Court stopped it. In 2021, the government drafted legislation to finish the job. Parliament never voted on it. Now, in 2026, leaked internal documents reveal the RBI has never abandoned the ambition — it has simply been waiting for the right moment.

The government still has a choice. The rest of the world chose regulation. India is contemplating the alternative. Whatever the final decision, 39 million investors deserve clarity — not eight more years of grey zone limbo while bureaucrats debate whether to protect them or eliminate their market entirely.

This is a developing story. Bullish Times will continue to track India’s crypto regulatory position as new information becomes available.