Polymarket — the platform that bills itself as “where markets seek truth” — is now being sued for allegedly rewriting the truth after traders already had the receipts. Two users filed suit in New York’s Supreme Court, claiming the prediction market giant resolved an $80 million bet as “No” despite an SEC filing proving the opposite.

The lawsuit, filed on 3 July 2026 by Burwick Law on behalf of traders William Wood and Thomas Bush, targets Adventure One QSS Inc., Blockratize Inc., CEO Shayne Coplan, and CMO Matthew Modabber. The complaint centres on a prediction market resolution that has sent shockwaves through the entire prediction market industry — and it could not have come at a worse time for Polymarket.

The $80 Million Bet That Went Wrong

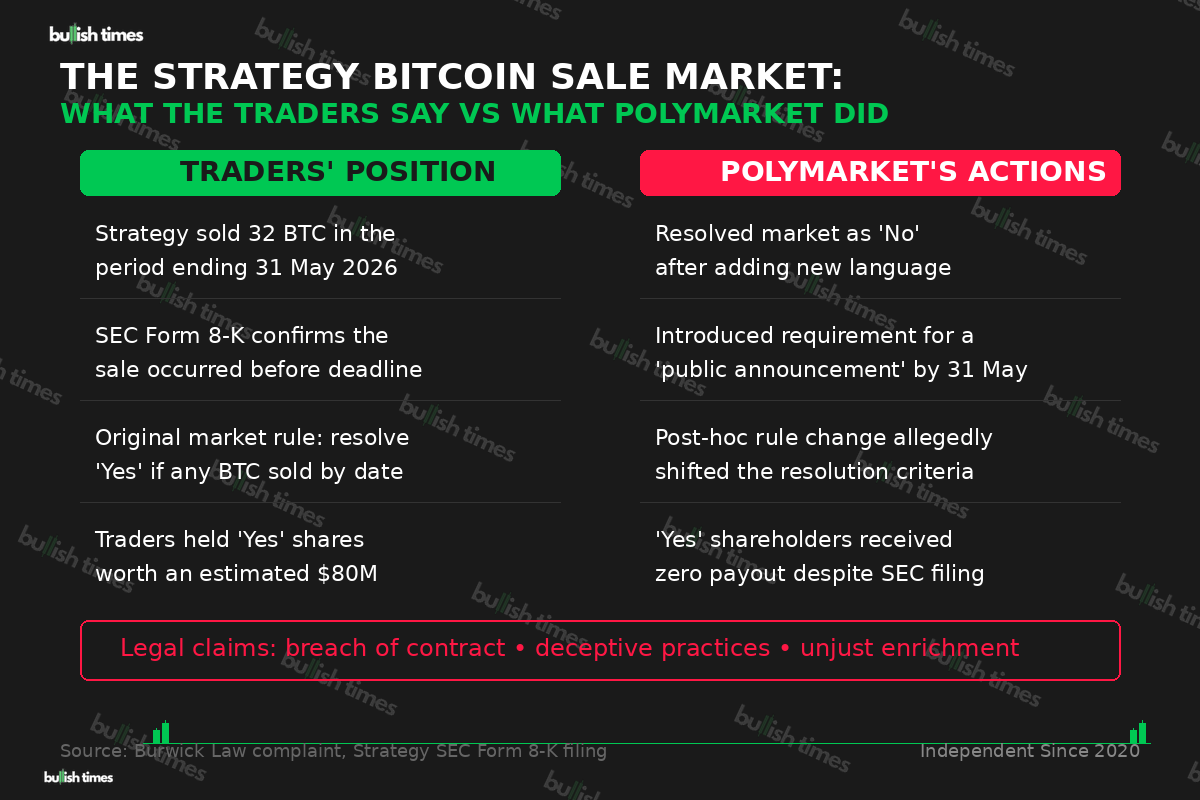

The Polymarket market in question asked a straightforward question: “Will Strategy (formerly MicroStrategy) sell any of its Bitcoin by 31 May 2026?” Traders placed roughly $80 million in wagers, and the plaintiffs backed “Yes.”

Here’s where it gets controversial. Strategy’s SEC Form 8-K filing disclosed the sale of 32 BTC during the period ending 31 May 2026. For most reasonable observers, that should have settled the matter.

But Polymarket didn’t see it that way.

According to the complaint, the platform resolved the market as “No” — and only after introducing additional language that allegedly changed the resolution standard entirely. The new requirement? A “public announcement” confirming the sale by the deadline. The SEC filing, apparently, didn’t count.

Post-Hoc Rule Changes and the Trust Crisis

The legal claims are damning. Burwick Law alleges breach of contract, breach of the implied covenant of good faith and fair dealing, unjust enrichment, deceptive acts and practices under New York GBL §§ 349 and 350, and false advertising. The plaintiffs seek damages, treble damages where available, injunctive relief, and attorneys’ fees.

The core allegation is that Polymarket engaged in what amounts to moving the goalposts after the game was already over. The market’s original rule stated it would resolve “Yes” if MicroStrategy sold any Bitcoin by 11:59 p.m. ET on the specified date. When the outcome became clear via Strategy’s own regulatory filing, the platform allegedly introduced a new criterion that hadn’t existed when traders placed their bets.

This isn’t just a contractual dispute. It strikes at the philosophical foundation of prediction markets: that outcomes are determined by pre-agreed, objective criteria, not by platform discretion.

A Pattern, Not an Isolated Incident

What makes this lawsuit particularly explosive is the context surrounding Polymarket right now. The platform is simultaneously navigating a perfect storm of legal, regulatory, and reputational crises that collectively raise serious questions about its operational integrity.

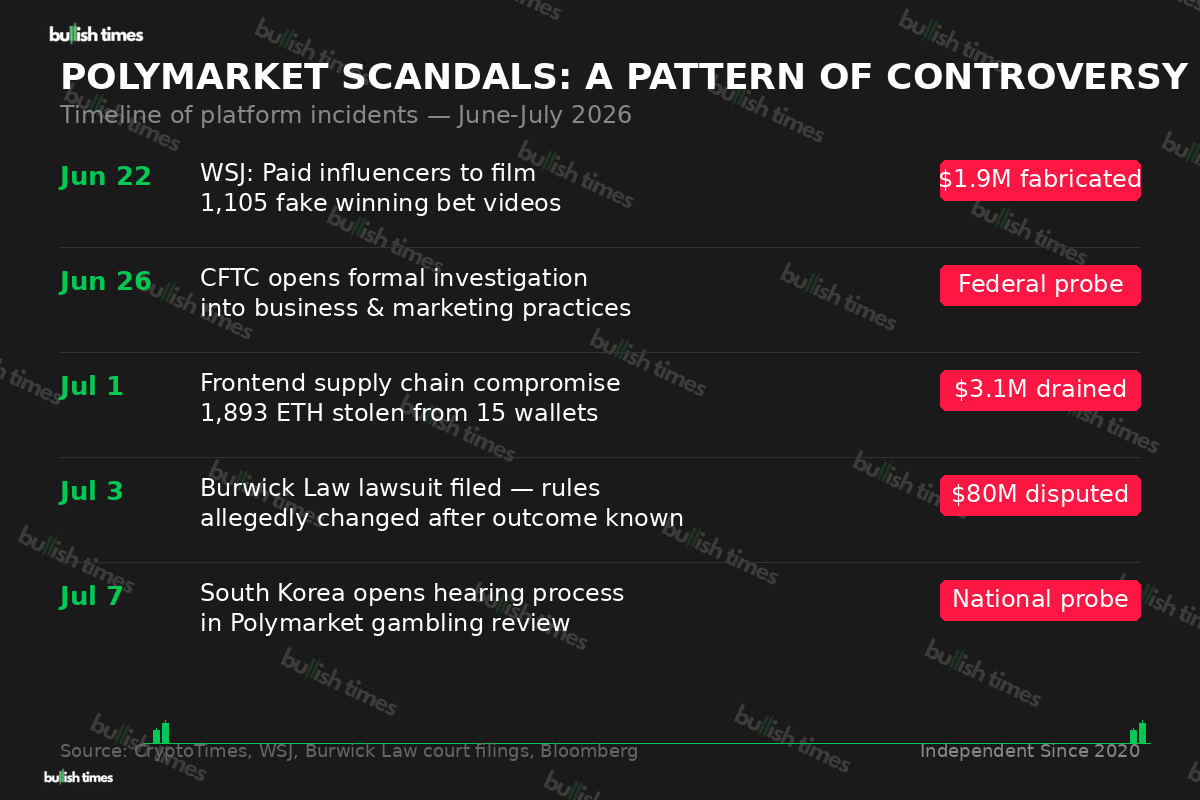

On 22 June, the Wall Street Journal revealed that Polymarket had paid social media creators to film staged trading videos — more than 1,100 clips featuring fabricated winning bets on fake websites, costing the platform an estimated $1.9 million. Days later, on 26 June, the CFTC confirmed it had opened a formal investigation into Polymarket’s business practices, with enforcement attorneys pushing the probe forward alongside the Department of Justice.

Then came the 1 July frontend compromise, in which attackers exploited a supply chain vulnerability to drain approximately $3.1 million in ETH from 15 user wallets. And South Korean authorities have launched a gambling probe targeting domestic Polymarket users, adding yet another jurisdictional headache.

Prediction Market Accountability Meets the Courtroom

Burwick Law describes this case as one of the first major lawsuits focused specifically on prediction market accountability and market resolution procedures. If the court rules in favour of the traders, it would establish a precedent that prediction market platforms cannot retroactively alter resolution criteria — a principle that seems obvious but has never been tested in court.

For Shayne Coplan and Polymarket, the stakes extend far beyond this single market. Polymarket processed $44.8 billion in volume in June alone, up 75% from May. But volume means nothing if traders cannot trust that the platform will honour the rules as written. The CFTC investigation, the deceptive marketing scandal, the frontend breach, and now a lawsuit alleging deliberate market manipulation — each one is damaging on its own. Together, they paint a portrait of a platform that has grown faster than its governance can handle.

The broader prediction market industry should be paying close attention. Kalshi, which is reportedly seeking a $40 billion valuation, will be watching to see whether regulators and courts begin drawing clearer lines around platform discretion in market resolution. If Polymarket loses this case, every prediction market operator will need to rethink how much unilateral power they hold over outcomes.

The real irony? Prediction markets are supposed to be the antidote to institutional bias — decentralised truth machines that aggregate collective intelligence without a central authority putting its thumb on the scale. If Polymarket truly changed the rules after the outcome was known, it did exactly what prediction markets were built to prevent.

This story is developing. The court has yet to rule on the complaint, and Polymarket has not publicly responded to the allegations. All claims are allegations at this stage.