Nine thousand seven hundred crypto ATMs went dark on Sunday night. No warning. No transition plan. Just silence — and a bankruptcy filing that reads like a confession.

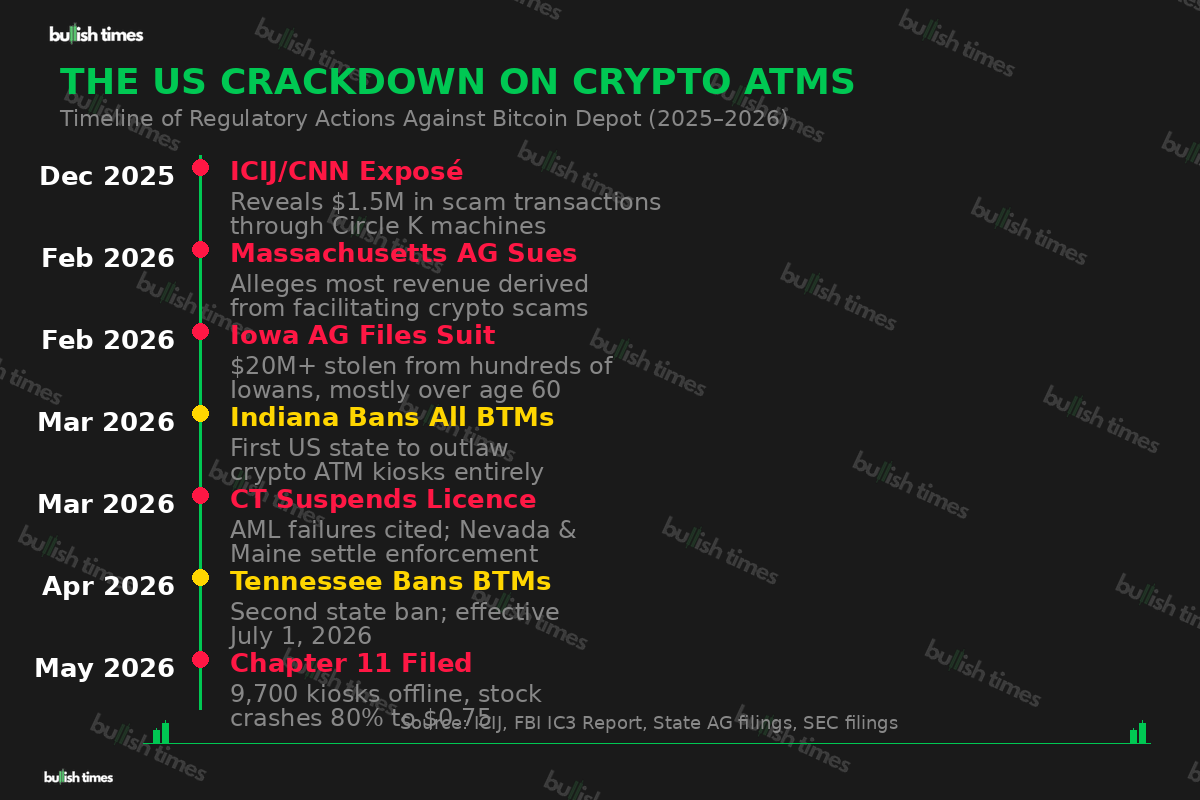

Bitcoin Depot, the company that once operated the largest network of cryptocurrency ATMs in North America, filed for voluntary Chapter 11 bankruptcy on 18 May 2026. The company’s stock cratered 80%, its entire kiosk network was switched off, and CEO Alex Holmes effectively admitted the business model was finished. But the real story isn’t the collapse itself — it’s what the company was profiting from all along.

The Numbers Don’t Lie

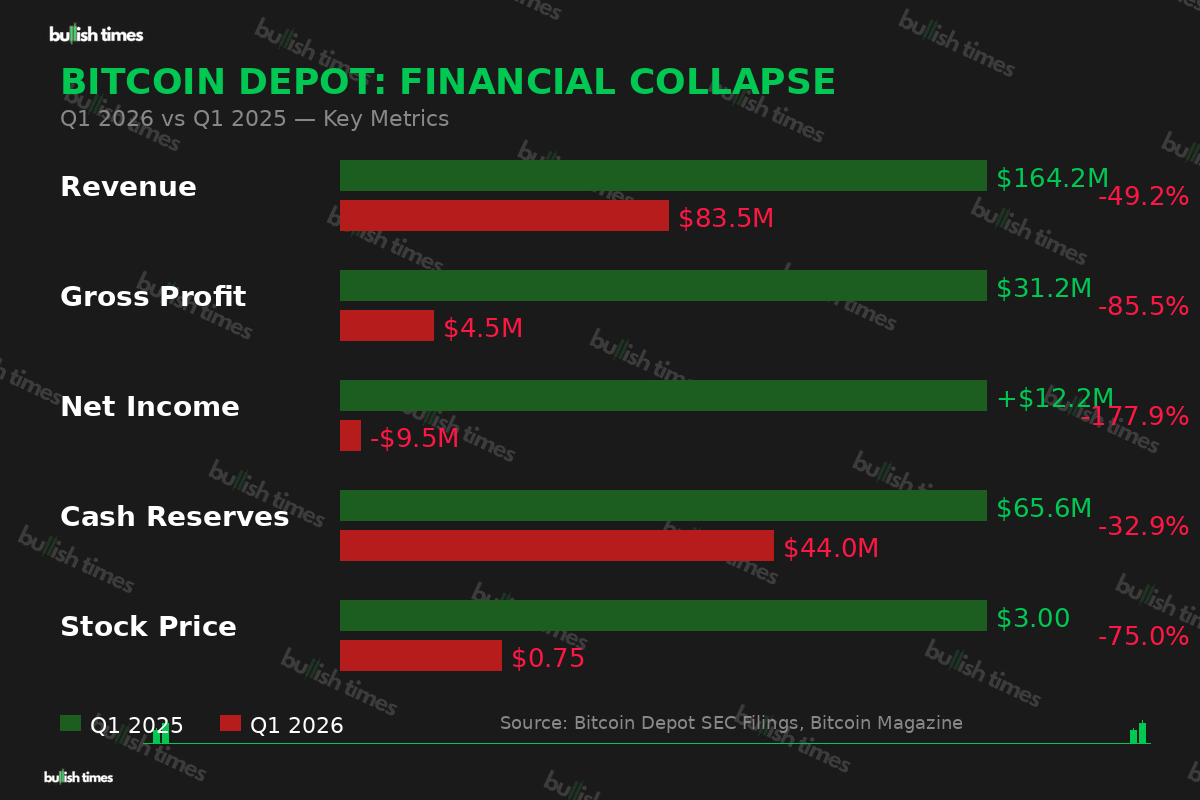

Bitcoin Depot’s implosion was spectacular even by crypto standards. Revenue plummeted 49.2% year-on-year in Q1 2026, falling from $164.2 million to just $83.5 million. Gross profit collapsed 85.5% — from $31.2 million to a skeletal $4.5 million. The company swung from a $12.2 million net profit to a $9.5 million net loss. Cash reserves haemorrhaged from $65.6 million to $44 million in three months.

The stock told the rest of the story. BTM shares fell from $3 to $0.75 on the announcement — an 80% wipeout that effectively vaporised whatever remained of shareholder value. The NASDAQ-listed company, which had gone public via SPAC in 2023 to considerable fanfare, was now preparing to liquidate.

A 23% Cut of Grandma’s Life Savings

Here’s where the story turns from corporate failure to moral catastrophe. The Iowa Attorney General’s investigation revealed that Bitcoin Depot was taking a 23% cut on every transaction processed through its machines. Twenty-three per cent. For context, a standard bank ATM charges around 2–3%.

But the fee structure was only part of the problem. The FBI logged 13,460 crypto-kiosk fraud complaints in 2025 alone, with reported losses of $389 million — a 58% surge from the prior year. Scammers had discovered that Bitcoin ATMs were the perfect extraction tool: convince a vulnerable victim (frequently elderly) that their bank account had been compromised, direct them to the nearest kiosk, and have them feed in cash that would be instantly converted to cryptocurrency and whisked offshore beyond the reach of law enforcement.

Massachusetts Attorney General Andrea Campbell didn’t mince words when she filed suit in February 2026, alleging that most of Bitcoin Depot’s revenue was derived from facilitating crypto scams. Iowa’s AG was equally blunt, noting that scammers “even hunt through obituaries to target widows” before sending victims to Bitcoin Depot machines.

A 2025 investigation by ICIJ and CNN found at least $1.5 million in confirmed scam transactions flowing through hundreds of Bitcoin Depot machines installed inside Circle K convenience stores. Circle K management was aware of the problem, the investigation found, but continued the partnership anyway — the rental fees were simply too lucrative to abandon.

The Regulatory Avalanche

The crackdown, when it finally came, was swift and devastating. Indiana became the first US state to outright ban crypto ATM kiosks in March 2026. Tennessee followed in April, with the ban set to take effect on 1 July. Minnesota joined the prohibition wave. Connecticut suspended Bitcoin Depot’s banking licence over anti-money laundering failures. Nevada and Maine forced settlement agreements with fines and compliance requirements.

Bitcoin Depot wasn’t merely facing regulatory headwinds — it was being systematically dismantled by the American legal system, state by state. The company racked up over $20 million in legal judgments during Q4 2025 alone, including a $19 million arbitration award related to its Canadian subsidiary. Operating expenses ballooned 32.3%, driven almost entirely by litigation costs.

The Leadership Carousel

The executive suite was its own circus. Founder Brandon Mintz, who built Bitcoin Depot from a University of Georgia dorm room into a NASDAQ-listed company with 9,000+ machines across 47 states, was quietly shifted to a “non-executive board” role in March 2026. His replacement as CEO, Scott Buchanan, lasted barely any time before departing to “pursue opportunities outside the firm” — corporate-speak for jumping ship before the hull split.

Enter Alex Holmes, a 16-year MoneyGram veteran who joined the board in August 2025 and was handed the CEO title just in time to preside over the collapse. Holmes’s statement accompanying the bankruptcy filing was remarkable in its candour: the company’s business model, he said, was simply “unsustainable.”

Restructuring adviser Roshan Dharia of Echo Base Global called the bankruptcy “a preview of what the broader crypto ATM industry will face” across America. “The traditional model depended on high transaction spreads and limited regulatory scrutiny,” he observed. That equation, he said, has now “broken down.”

What Happens Next — And What This Really Means

Bitcoin Depot’s collapse raises a question that the crypto industry has spent years dodging: when does “financial access” become a euphemism for enabling fraud?

The company’s defenders will argue it was simply a cash-to-crypto on-ramp — a service for the unbanked, a tool for financial inclusion. But the data tells a different story. When your attorney general alleges that the majority of your revenue flows from scam-related transactions, when the FBI is logging nearly $400 million in annual fraud losses through your machines, when you’re taking a 23% spread that dwarfs anything in traditional finance — the “financial inclusion” narrative doesn’t hold up to scrutiny.

Canada is now considering its own nationwide ban on crypto ATMs. The remaining US operators — DigitalMint, CoinFlip, Coinme — will face the same regulatory gauntlet that destroyed Bitcoin Depot. The entire sector, which exploded from a few hundred machines in 2018 to over 38,000 at its peak in 2024, is now contracting rapidly.

There’s a bitter irony here. Bitcoin was designed to eliminate the need for trusted intermediaries. Instead, Bitcoin Depot became the worst kind of intermediary: one that extracted 23% from every transaction while providing a frictionless pipeline for fraud. The technology was neutral. The business model was not.

Bitcoin Depot’s Chapter 11 proceedings are ongoing in the US Bankruptcy Court for the Southern District of Texas. The company’s 9,700 kiosks remain offline, and a full asset liquidation is expected in the coming months.