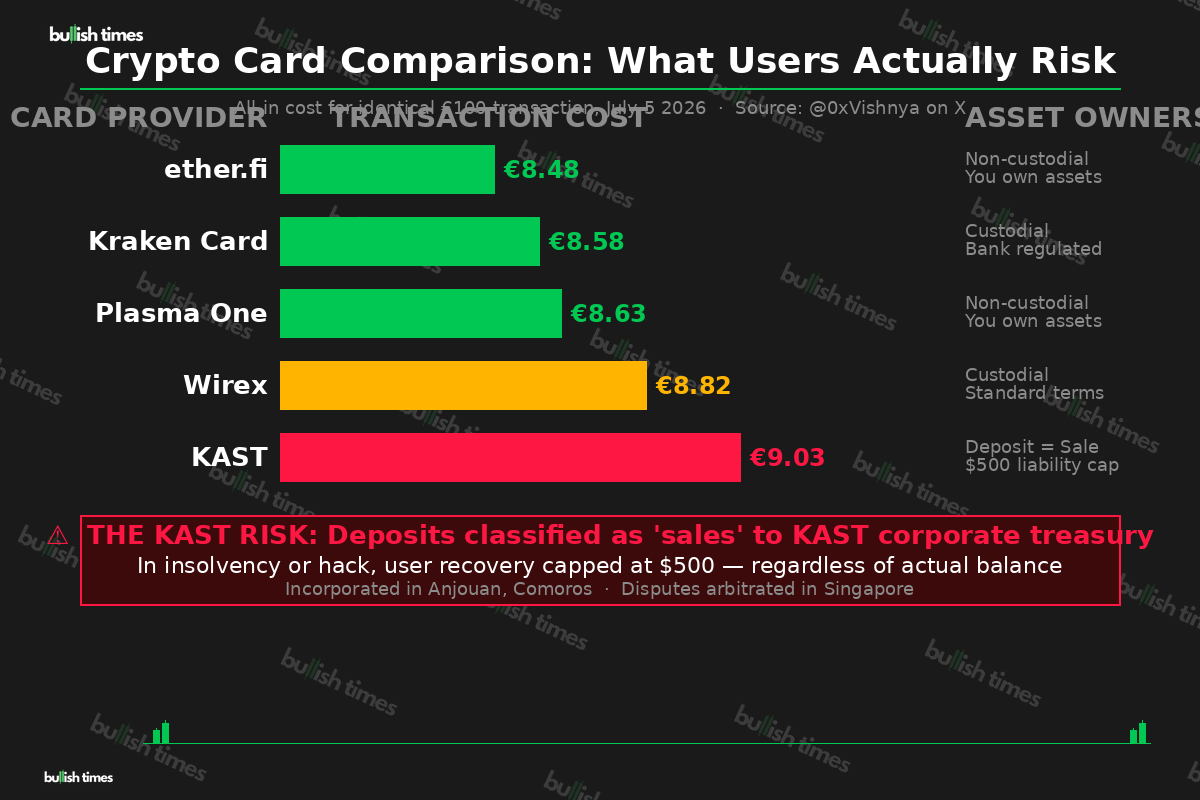

You think you’re loading up a crypto card. You’re actually selling your assets to a $600 million company — and if it all goes wrong, you’re legally entitled to $500.

That is the stark reality buried inside KAST’s Terms of Service, and it took a rival CEO calling the company a “Kasthole scammer” on X for most users to notice it was there.

The Fine Print That Changed Everything

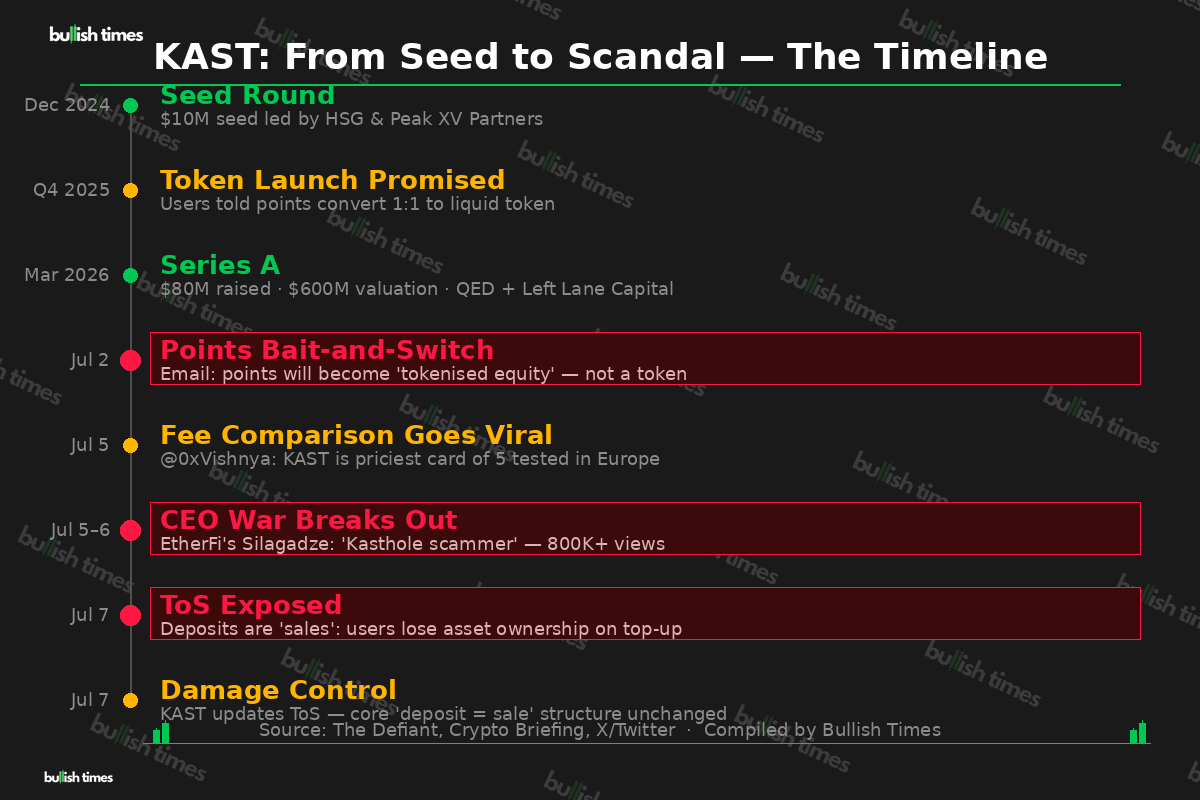

KAST is a Singapore-and-UAE-based crypto neobank that raised $80 million in a Series A round in March 2026 at a $600 million valuation — backed by QED Investors, Left Lane Capital, and following a $10 million seed in December 2024. On paper, it offers a slick stablecoin card for spending crypto in 100-plus countries. In practice, its Terms of Service have been quietly structured around a legal principle that most users never saw coming.

The clause, verified against KAST’s own website as recently as 25 June 2026 by The Defiant using the Wayback Machine, reads: “When a user transfers Virtual Assets (such as cryptocurrencies or stablecoins) into KAST, the transfer is treated as a sale of the Virtual Asset to KAST. For clarity, once a user sells their Virtual Assets to KAST, the user no longer retains any ownership interest in those Virtual Assets. Ownership of the Virtual Assets transfers to KAST, and the assets are thereafter managed at the KAST corporate treasury level.”

That is not custody. That is ownership transfer. The moment your stablecoins hit KAST, they belong to the company. The same section caps total liability to users at $500 — regardless of actual balance — and incorporates the company in Anjouan, Comoros, with disputes governed by Seychelles law and arbitrated in Singapore.

The Fight That Exposed It All

The ToS would likely have stayed buried had ether.fi CEO Mike Silagadze not gone to war with KAST CEO Raagulan Pathy in public. It started on 5 July when pseudonymous trader @0xVishnya posted a real-world comparison of five crypto cards used for an identical purchase in Europe. KAST came in last — the most expensive at €9.03 all-in, versus €8.48 for ether.fi. Silagadze quote-tweeted it within seven minutes, boasting about ether.fi’s fees and superior product.

Pathy hit back with a chart of ether.fi’s own token, ETHFI — down 95% from its 2025 all-time high of $8.53 — captioning it with a sarcastic remark about Silagadze’s marketing bravado. Silagadze escalated: “Your whole business is scamming your customers. You’re a con artist.” Pathy responded with a South Park GIF. Silagadze posted “Kasthole scammer” — and the post gathered 800-plus likes and north of 400,000 views within hours.

The community started digging. What they found was the ToS clause above. Investor Simon Dedic pointed out that the deposit structure creates a taxable event for users on top of losing asset ownership. Trader Matt Casto noted that KAST had incentivised card spending to earn point multipliers — right before announcing those same points would no longer convert to a liquid token.

That last part matters. KAST had originally promised a token-generation event in Q4 2025, then pushed it to Q2/Q3 2026. On 2 July, users received an email: their points would convert to “tokenised equity” instead — meaning an illiquid stake in the company, not a tradeable token. The timing, just months after the $80 million raise closed, raised immediate questions.

Why the Structure Exists — and Why That’s the Problem

KAST’s model is not entirely without logic. Because incoming stablecoins are booked as company assets rather than customer deposits, KAST can earn yield on idle balances — estimated at 4–5% annually on T-bill-backed instruments. Competitors such as ether.fi, Plasma, and Avici settle transactions through user-controlled smart contracts or licensed banking partners, meaning they cannot monetise balances in the same way. KAST can. And at scale, that yield is meaningful.

The problem is the risk asymmetry. A traditional bank deposit in the UK or US carries regulatory protections — FSCS coverage up to £85,000, FDIC insurance up to $250,000. KAST’s structure offers neither. It is incorporated in Anjouan, Comoros — a jurisdiction not widely known for its consumer financial regulation. The $500 liability cap is not a rounding error; it is the entire safety net.

KAST updated its ToS on 7 July, adding language confirming that users retain a right to redeem unspent balances. But the fundamental structure did not change — deposits are still classified as sales, ownership still transfers. The update addressed the optics, not the underlying mechanics. And because the company’s own CEO, Raagulan Pathy, confirmed on X that funds are held with BitGo and Fireblocks, the question of why the deposit-as-sale structure is legally necessary at all remains unanswered.

What Comes Next

KAST is not the first crypto card to carry aggressive deposit terms — and it almost certainly will not be the last. But the feud made this one impossible to ignore, and the community’s response has been swift. Several users have already announced they have switched to non-custodial alternatives. The pressure on Pathy to provide a clearer structural solution — not just an amended ToS — is unlikely to ease.

The deeper issue is what this episode reveals about how quickly a $600 million valuation can be built on a product that most of its users did not fully understand. KAST’s Series A happened just four months ago. The deposit terms have been in place for longer than that.

The custodial vs. non-custodial debate is not new in crypto. But this is one of the clearest illustrations yet of why the distinction matters — not in theory, but in the fine print of a card you use to buy coffee.

This story is developing. KAST has been contacted for further comment. Bullish Times will update if a structural response is provided.