“Never. No. We’re not sellers. We’re only acquiring and holding BTC.” That was Michael Saylor’s solemn vow to Bloomberg. On 1 June 2026, Strategy’s SEC filing proved those words have an expiry date.

For five years, Saylor built an identity — not just a corporate treasury — around one unbreakable rule: buy Bitcoin, never sell. The laser eyes, the podcast sermons, the “sell a kidney before you sell your Bitcoin” quips. It wasn’t just a strategy. It was a religion. And on Sunday evening, Strategy’s 8-K filing quietly confirmed that the church had sold the communion wine.

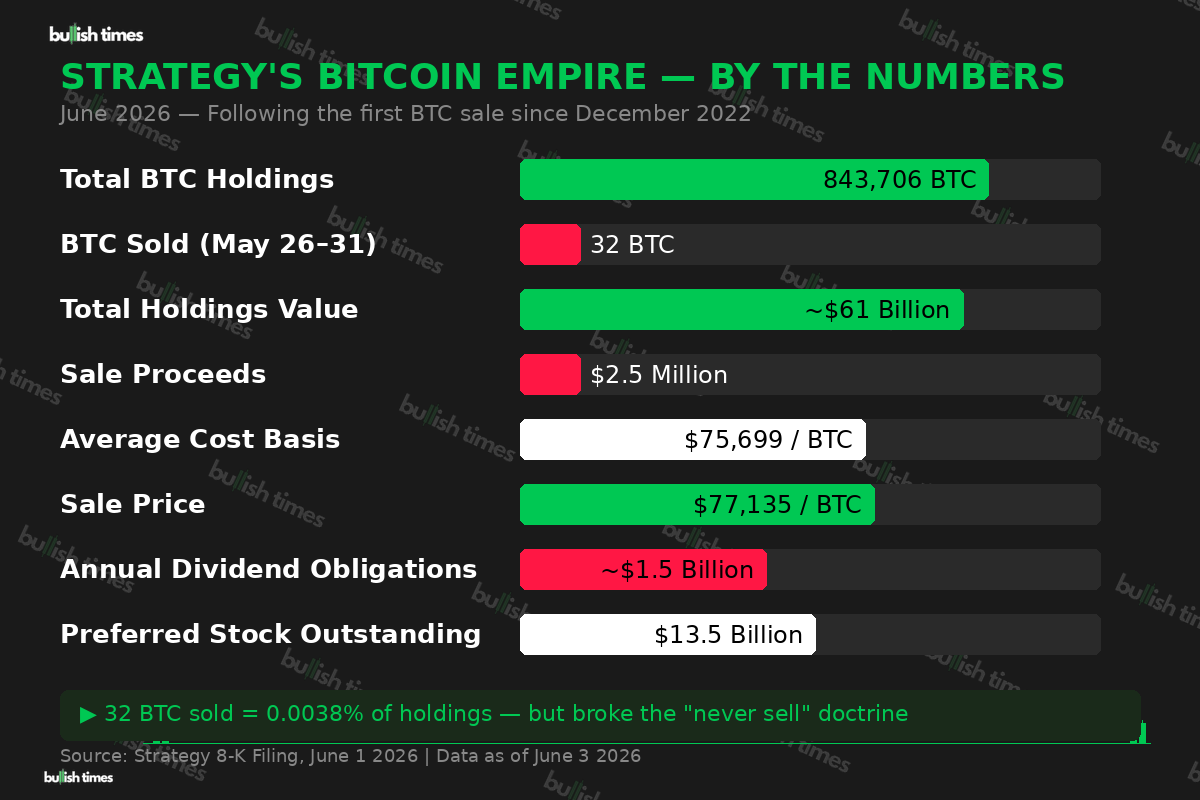

Thirty-Two Coins That Shook a $61 Billion Stack

Between 26 and 31 May, Strategy sold 32 BTC at an average price of $77,135 per coin, raising approximately $2.5 million. In absolute terms, this is laughably small — 0.0038% of the company’s 843,706 BTC holdings, worth roughly $61 billion. Strategy’s average cost basis sits at $75,699 per coin, meaning the sale scraped a 1.9% profit.

But arithmetic isn’t the point. Doctrine is.

The proceeds fund distributions on Strategy’s preferred stock. CEO Phong Le had telegraphed the possibility on the Q1 earnings call, and Saylor himself floated it as a way to “inoculate” markets against future shock. The inoculation didn’t work. MSTR shares cratered 5.85% on Monday. Bitcoin slid 2%, briefly touching its lowest level since mid-April. More than $93 million in futures positions were liquidated in a single hour — 95% of them longs.

The Dividend Machine That Cracked the Doctrine

Strategy is now the world’s largest issuer of what it brands “Digital Credit” — more than $13.5 billion in preferred equity across five series, headlined by STRC at 11.50% annual dividend ($8.5 billion in nine months). Total annual dividend obligations: roughly $1.5 billion, payable whether Bitcoin is at $100,000 or $50,000. The company has met 23 consecutive distributions totalling over $693 million.

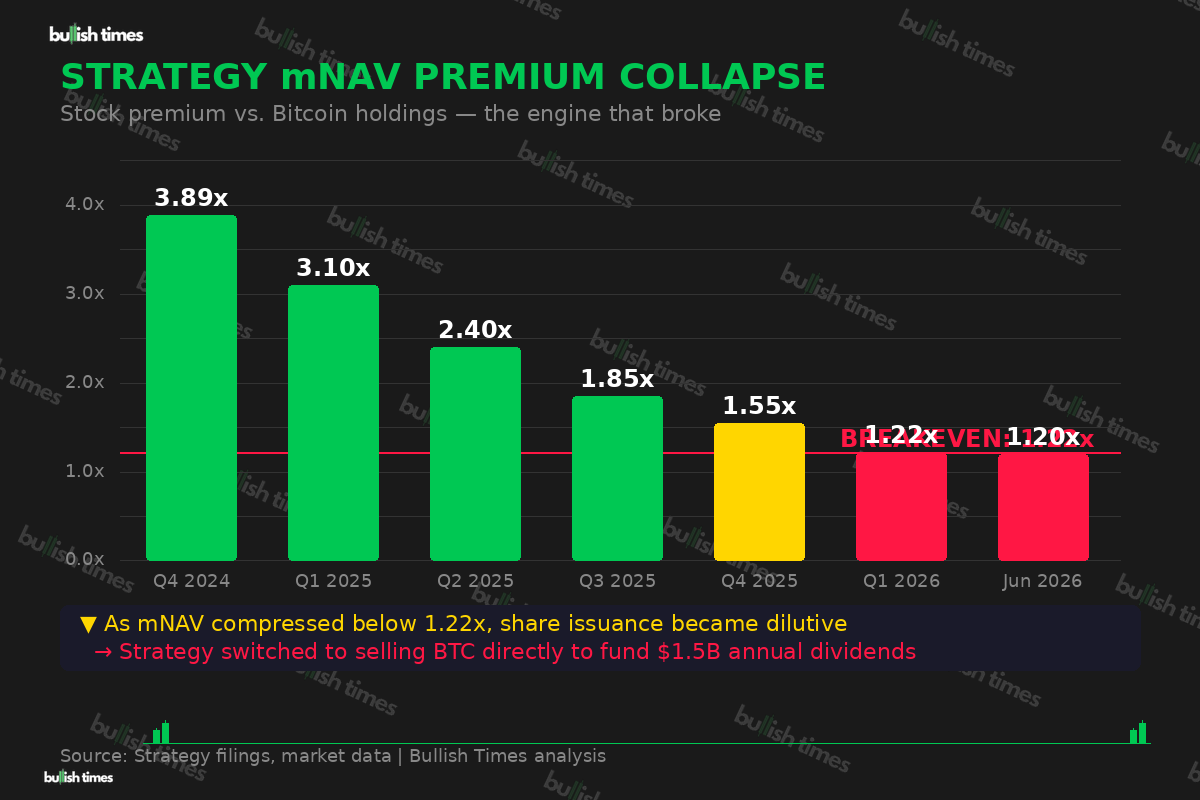

Normally, these are funded by issuing new MSTR common shares. That works when the stock trades at a fat premium to underlying Bitcoin — a ratio tracked as mNAV. The breakeven sits at approximately 1.22x. Above that, selling shares is accretive. Below it, every share sold dilutes holders.

The problem: mNAV has collapsed from 3.89x in late 2024 to roughly 1.2x — right at breakeven. When the premium gets that thin, the share-issuance engine sputters. Strategy reached for the only other lever: selling Bitcoin directly.

The Polymarket Chaos Nobody Expected

The sale also triggered a sprawling dispute on Polymarket, where more than $80 million had been wagered on whether Strategy would sell Bitcoin by 31 May. The sale occurred within the deadline, but wasn’t disclosed until 1 June. Polymarket initially proposed resolving the market as “No,” arguing there was no public confirmation before expiry.

“Polymarket should trade truth, not technicalities,” one furious bettor wrote. Two proposed resolutions have been challenged, and the final decision now rests with UMA token holders. A prediction market built on objective truth can’t agree on whether a sale that provably happened actually happened. Even reality’s referees are struggling.

The Copycats Should Be Nervous

Strategy inspired an entire movement of corporate Bitcoin treasuries — from Metaplanet in Japan to dozens of smaller firms that adopted the Saylor playbook. If the original architect is now selectively liquidating, it gives every copycat permission to do the same.

Saylor has reframed the doctrine around “Bitcoin per share” (BPS) — arguing that selective sales can protect per-share value. It’s clever. It may be mathematically sound. But it’s fundamentally different from “we will never sell.” The unconditional buyer has become a conditional one.

What Happens Next

Strategy insists it has 18 months of dividend coverage, backed by $26 billion in remaining share-issuance capacity. The 32-coin sale was flagged in advance, executed at a small profit, and funded a specific obligation.

But markets don’t trade on spreadsheets alone. They trade on narratives — and “never sell” was the single most powerful narrative in corporate Bitcoin. Its death forces a repricing of what Strategy is: not a passive Bitcoin vault, but a leveraged financial machine with $1.5 billion in annual obligations and a willingness to liquidate its core asset when the maths demands it.

The number to watch isn’t 32 BTC. It’s mNAV. If the premium recovers, the share-issuance engine restarts and Bitcoin sales stop. If it compresses further, the world’s largest corporate holder becomes a price-sensitive seller during weakness. That’s a structural shift the market has never had to price before.

Saylor told CoinDesk on 11 May that for every Bitcoin Strategy sells, it would buy 20. We’ll be watching. Developing story.