The most powerful financial network on the planet just went blockchain. The crypto community should be celebrating — and also very, very worried.

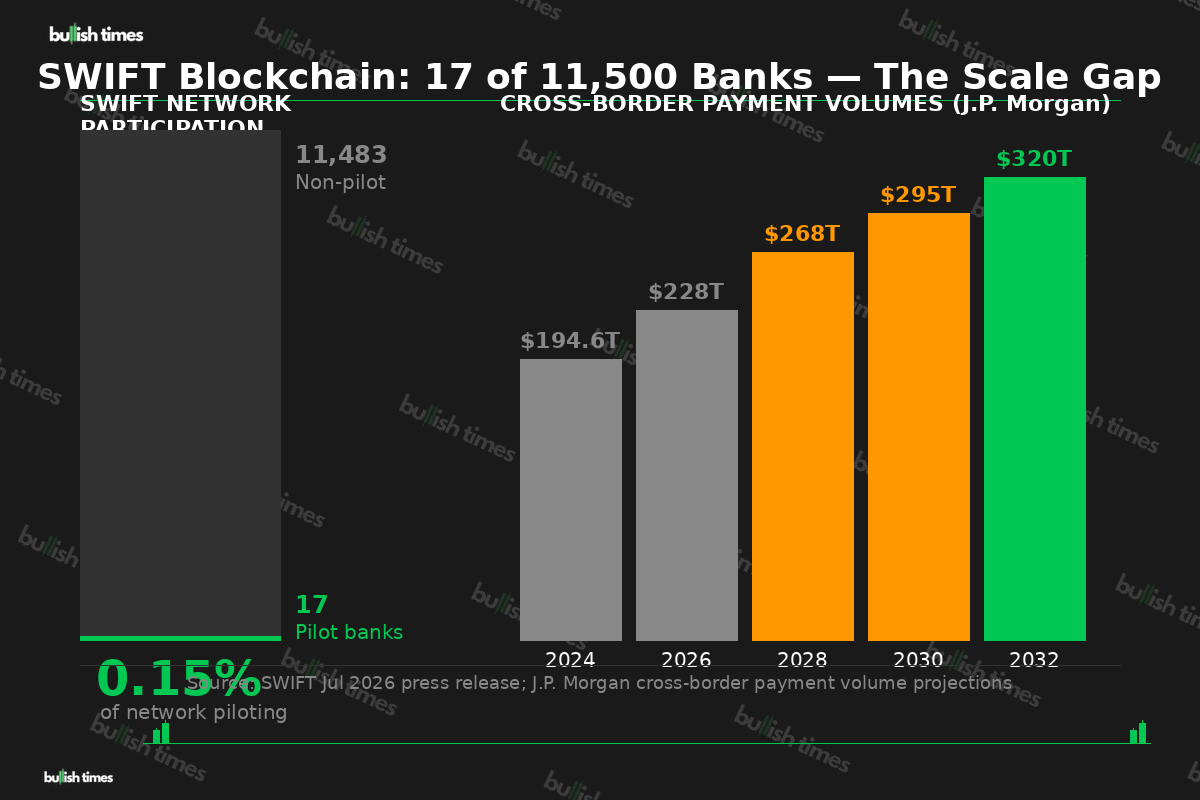

On 9 July 2026, SWIFT officially launched its blockchain-based shared ledger, announcing that 17 banks from six continents are preparing to pilot live transactions using tokenised deposits for 24/7 cross-border payments. The names on the list read like a who’s who of global finance: HSBC, Citi, UBS, Wells Fargo, BNP Paribas, BNY, Standard Chartered, Lloyds Bank. In nine months flat, SWIFT moved from concept to live infrastructure — a pace that would make most crypto protocols blush.

The question is not whether SWIFT’s entry into blockchain matters. It unquestionably does. The question is whether this is crypto’s ultimate vindication — or its most dangerous competitive threat to date.

What SWIFT Actually Built

Let us be clear about what SWIFT’s blockchain-based ledger is and, critically, what it is not.

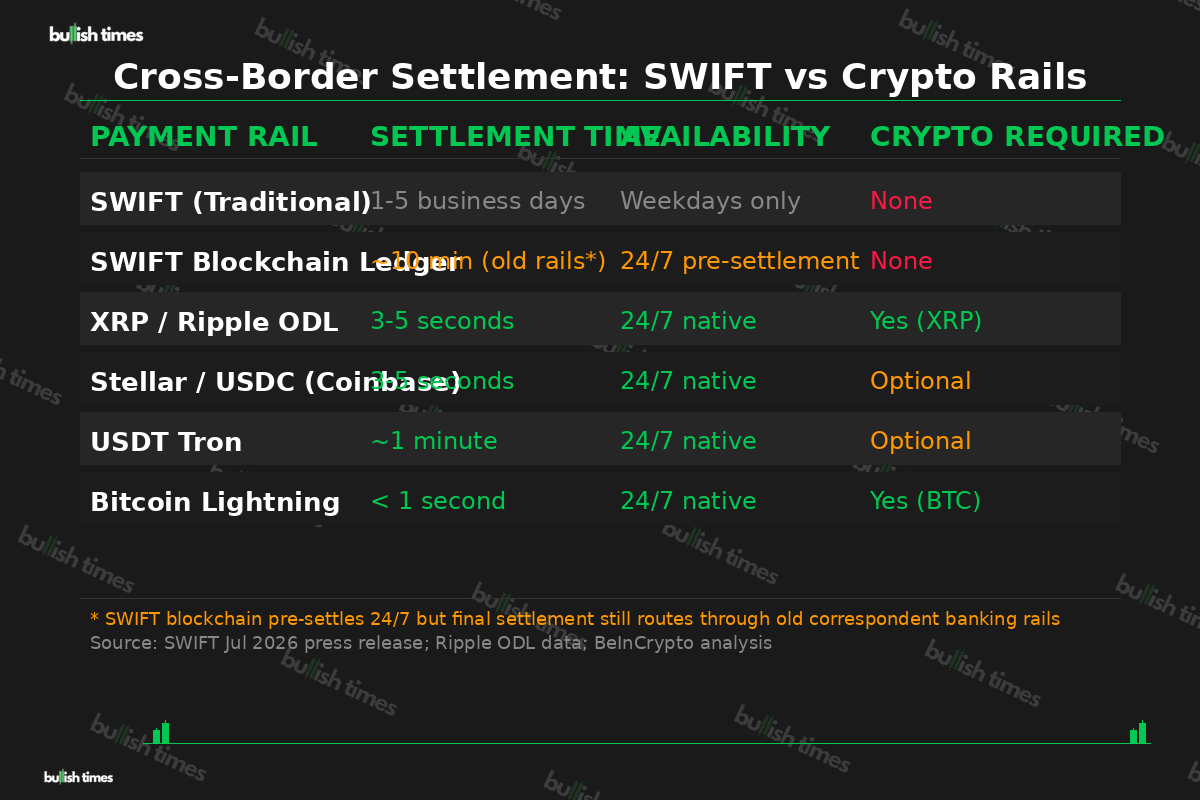

SWIFT built the system on Linea, ConsenSys’s Ethereum Layer-2 network, using a Hyperledger Besu-based EVM-compatible model. But access is fully permissioned. Only the bank consortium controls who can transact. No open validators. No permissionless participation. No decentralisation.

The ledger acts as an orchestration layer for tokenised deposits — digital versions of commercial bank money. Banks can move funds overnight and on weekends, with pre-settlement happening on the blockchain. The catch? Final settlement still routes through SWIFT’s existing correspondent banking rails. The SWIFT permissioned blockchain does not replace the infrastructure; it sits on top of it.

That is a crucial distinction. SWIFT itself acknowledges that 75% of payments on its existing network already reach beneficiary banks within ten minutes. The new ledger adds 24/7 availability for pre-settlement — but does not change the underlying settlement finality mechanism.

In the blunt assessment of BeInCrypto: “The ledger works as an orchestration layer, not a settlement replacement.”

The Irony Is Rich

SWIFT’s permissioned blockchain launch drips with irony for anyone who’s watched this space for more than a decade.

This is the same network that spent years questioning public blockchain infrastructure. SWIFT executives previously cast doubt on the XRP Ledger’s validator trust model. Now SWIFT has built a system that sidesteps that debate entirely — by keeping governance locked inside a closed bank consortium rather than distributing it across independent validators.

Meanwhile, public stablecoin rails have been processing 24/7 cross-border payments for years without needing 30 banks to spend nine months building shared infrastructure. MoneyGram on Stellar, Coinbase’s stablecoin payments network via Nium, the UAE’s dirham-backed stablecoin — all operational. All open. None requiring a membership card to participate.

The $320 Trillion Prize — And Who Controls It

Here is why this matters at civilisational scale. Cross-border payment volumes currently stand at roughly $194.6 trillion annually. J.P. Morgan projects that figure will reach $320 trillion by 2032. The global financial plumbing handling that volume is worth more than any individual crypto asset.

SWIFT’s 17-bank pilot represents just 0.15% of its 11,500-member network. But those 17 institutions are among the largest correspondent banks in the world. If this scales to hundreds of members, SWIFT will have created a tokenised settlement layer touching the majority of global institutional payment flows.

The XRP community is understandably divided. TipRanks called the launch “XRP’s worst nightmare,” arguing that if legacy banks can handle 24/7 transfers on infrastructure they already own, the utility case for Ripple’s On-Demand Liquidity weakens materially. SWIFT covers approximately $150 trillion in associated annual transaction value. Ripple’s cumulative institutional payment volume sits at roughly $95 billion total — a fraction of a single day on SWIFT’s rails.

But bulls counter that at least 30 of the 50-plus banks in SWIFT’s broader framework already have ties to Ripple’s ecosystem — and roughly 40% use ODL, which requires XRP as a bridge asset. The argument: XRP does not need to replace SWIFT; it can serve as liquidity infrastructure inside it.

The Walled Garden Problem

The deeper concern is not speed or settlement finality. It is who controls the rails.

SWIFT has historically been weaponised as a sanctions instrument. Russia’s disconnection in 2022 demonstrated that the network is not neutral infrastructure — it is a geopolitical tool operated by a Western-dominated cooperative. The new blockchain does not change that governance model. A permissioned ledger controlled by the same consortium retains the same powers of exclusion.

Crypto’s foundational promise was permissionless access — the ability for anyone, anywhere, to transact without needing institutional approval. What SWIFT has built is the antithesis: blockchain technology deployed to preserve institutional control, compliance oversight, and the existing correspondent banking hierarchy.

When Thierry Chilosi, SWIFT’s Chief Business Officer, says the ledger extends “the trust and stability of established finance into the frontiers of digital money,” one question remains unanswered: whose trust? The same institutions that excluded billions from the global financial system?

What Happens Next

More than 50 banks have joined SWIFT’s broader payments framework, with 25-plus expected to go live during 2026. The roadmap includes support for CBDCs, programmable money, and what SWIFT calls “agentic commerce” — AI-driven financial transactions that will require instant, borderless settlement.

SWIFT is positioning its blockchain as the institutional layer for that future, wrapping the technology in a compliance-friendly, access-controlled package. The cross-border payments boom to $320 trillion by 2032 is the prize.

The crypto sector built the blueprint. SWIFT just filed the building permit — for a gated community.

This is a developing story. The scale and pace of bank participation over the coming months will determine whether SWIFT’s permissioned blockchain becomes the dominant layer for institutional digital settlement — or a legacy institution’s last attempt to stay relevant.